|

|

| Monday, December 17, 2018 |

|

|

| Use the links below to navigate the report |

| ﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉﹉ |

|

|

|

|

|

|

| Benchmark carbon futures have more than doubled this year and just hit a 10-year high, buoyed by EU regulations effective next year that will cut away the number of carbon credit permits used by utilities and industrial polluters to cover their greenhouse gas emissions.

The resultant supply squeeze could push up European gas prices, which are already trading at the highest level for the time of the year in at least two decades.

Read More + |

|

|

| |

|

|

| Change-Driven Themes: Updates on Previous Featured Topics |

|

|

| Finance |

| Fintech Robinhood, the start-up upending stock trading, goes after banks with 3% checking and savings accounts |

| Read More + |

|

|

| Construction & Real Estate |

| Housing THEME ALERT Trouble in Housing? It’s More 1994 Than 2007 |

| Read More + |

|

|

| Services |

| Cannabis In the Wild West of pot stocks, U.S. companies create a Green Rush |

| eCommerce California lays out new e-commerce tax requirements |

| Travel Britons must pay €7 to visit mainland Europe after Brexit |

| Read More + |

|

|

| Energy & Environment |

| Energy Blockchain Scientists Say Blockchain ‘Delivering on Energy Promises’ |

| Wind More Than 680 Gigawatts Of New Wind Power To Come Online By 2027 |

| Read More + |

|

|

|

|

| |

| Joe Mac's Market Viewpoint |

|

|

|

|

| If you haven't signed up for website access already, see the bottom of the report for a how-to |

|

|

| The Next Handle → Stocks and bonds have struggled over the last year as yields have risen strongly, but MRP believes this is only the beginning. Further tightening of monetary policy is expected to continue delivering upward pressure on yields as slowing earnings and GDP growth begin to bite.

Joe Mac's Market Viewpoint: The Next Handle → |

|

|

|

|

|

|

|

|

| Select a theme to see recent Featured Topics we've written about it |

|

|

| If you haven't signed up for website access already, see the bottom of the report for a how-to |

|

|

|

|

|

|

|

|

|

|

| US Business Inventories Match Forecasts

Business inventories in the United States increased 0.6 percent month-over-month in October of 2018, following an upwardly revised 0.5 percent rise in September and in line with market expectations. Retail inventories excluding autos, which go into the calculation of GDP, jumped 0.7 percent after falling 0.1 percent in September. TE |

|

|

| US Services Activity Growth Eases to 11-Month Low

The IHS Markit US Services PMI fell to 53.4 in December 2018 from 54.7 in the previous month and well below market expectations of 54.7, a preliminary estimate showed. The latest reading pointed to the weakest pace of expansion in the service sector since January as new work rose the least since April 2017 and unfinished business fell for the first time in four months. On the price front, average cost burdens increased at the slowest rate for one year. TE |

|

|

| US Retail Sales Rise 0.2% in November

US retail trade rose by 0.2 percent from a month earlier in November 2018, following a revised 1.1 percent growth in October and matching market expectations. Retail sales excluding automobiles, gasoline, building materials and food services surged 0.9 percent in November after an upwardly revised 0.7 percent increase in October. TE |

|

|

| US Private Sector Expands the Least in 19 Months

The IHS Markit US Composite PMI dropped to 53.6 in December 2018 from 54.7 in the previous month, a preliminary estimate showed. The latest reading signaled the weakest expansion in private sector since May 2017 as services growth was the weakest in 11 months (PMI at 53.4 vs 54.7 in November) and manufacturing increased the least since November 2017 (PMI at 53.9 vs 55.3 in November). TE |

|

|

| US Factory Growth Lowest in Over a Year

The IHS Markit US Manufacturing PMI fell to 53.9 in December of 2018 from 55.3 in November, below market expectations of 55.1. The reading pointed to the slowest expansion in factory activity since November of 2017, as new orders and employment rose at a slower pace, preliminary estimates showed. Also, the near-term outlook has become less favourable. TE |

|

|

| US Industrial Output Rebound Beats Forecasts

US industrial output rose 0.6 percent from a month earlier in November 2018, following a downwardly revised 0.2 percent contraction in October and beating market expectations of a 0.3 percent gain. Mining and utilities output led the increase while manufacturing production was unchanged. TE |

|

|

| Sterling Weakens after EU Summit

The British pound fell against the USD on Friday after the first day of the EU summit on Thursday ended with the European Union saying the Brexit deal is not open for renegotiation. During the summit, the British Prime Minister made some proposals to the EU in order to address domestic critics, namely regarding the Irish backstop. The sterling was down 0.6% to $1.25882 around 11:10 AM London time. TE |

|

|

|

|

|

|

|

|

| If you haven't signed up for website access already, see the bottom of the report for a how-to |

|

|

| |

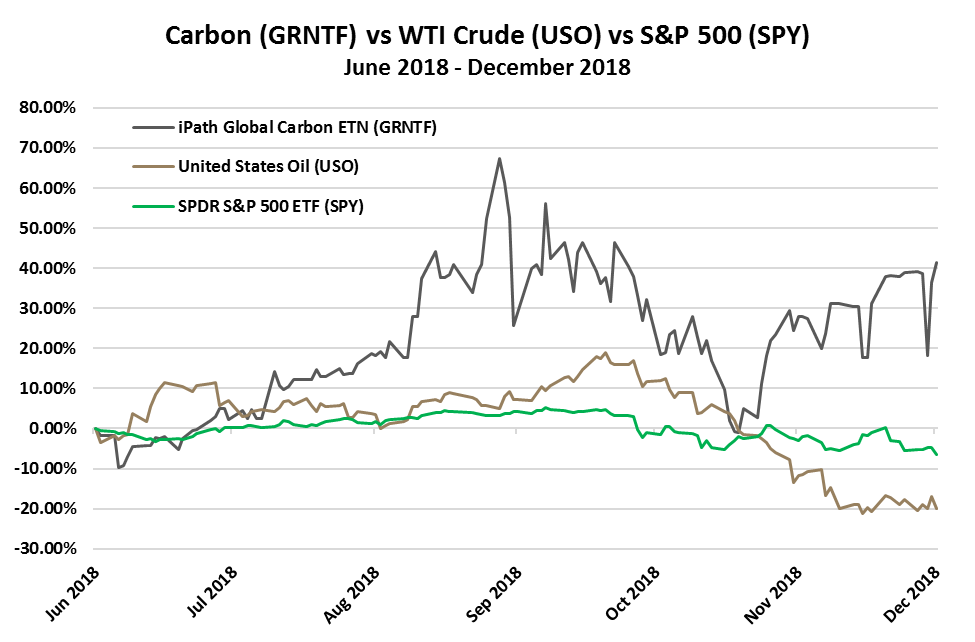

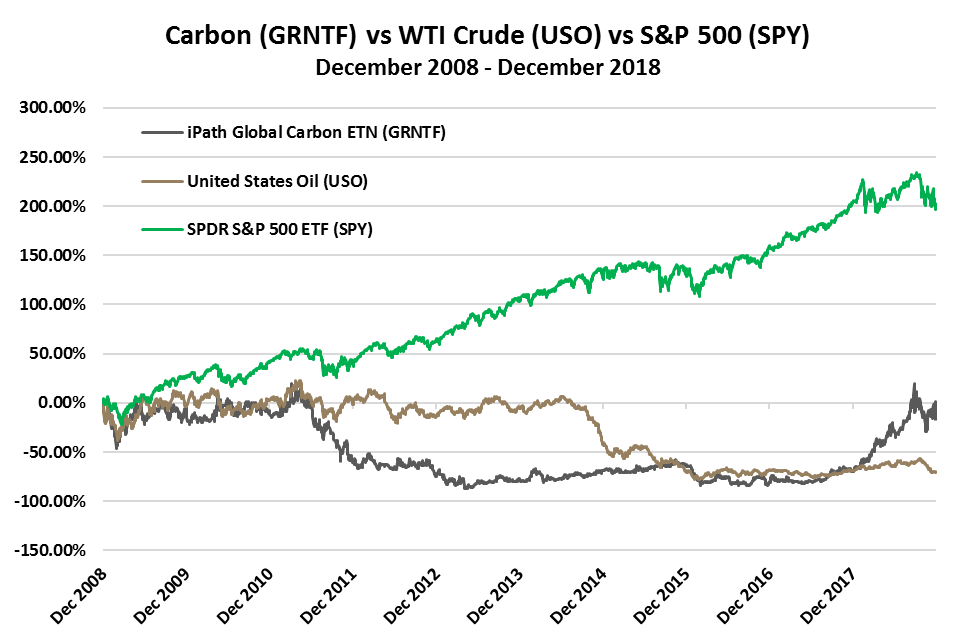

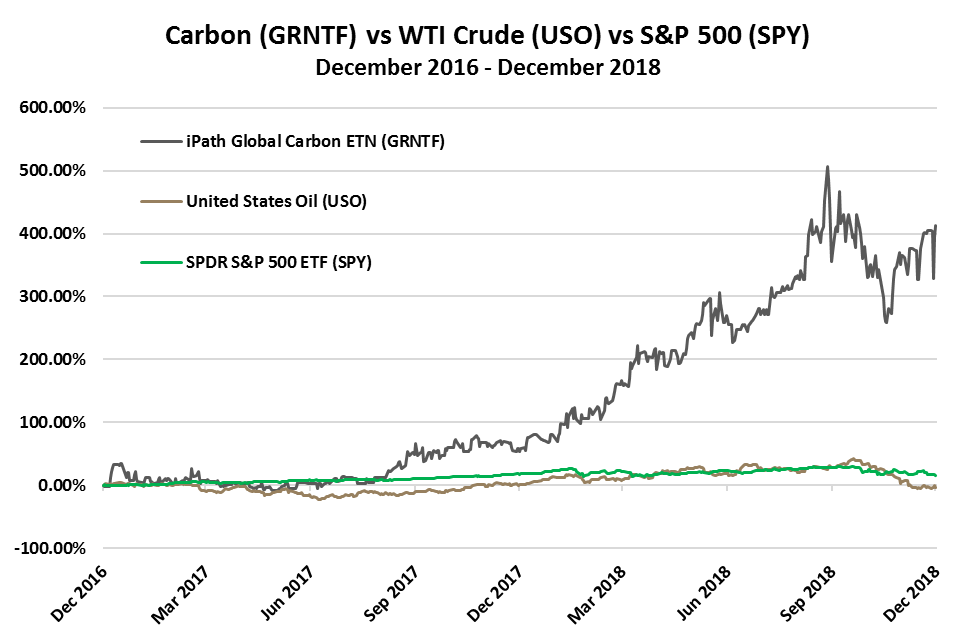

| Carbon Credit Prices Could Double, Pushing Gas Prices Up as Well → |

|

|

| Summary: Benchmark carbon futures have more than doubled this year and just hit a 10-year high, buoyed by EU regulations effective next year that will reduce the number of carbon credit permits used by utilities and industrial polluters to cover their greenhouse gas emissions. The resultant supply squeeze could push up European gas prices, which are already trading at the highest level for the time of the year in at least two decades. |

|

|

| While there’s plenty of debate around the issue of global warming, for those who believe it is real and imperiling our way of life, the general theory goes that excessive carbon emissions are the cause. With carbon dioxide levels at all-time highs, regulators at the United Nations are calling for stricter emission curbs in the form of much higher carbon taxes to stave off the worst effects of climate change.

Under the 1997 Kyoto Protocol and the more recent Paris Accord, governments and industrial companies are subject to annual quotas (a cap) on how much greenhouse gases (GHGs) they can emit. On this matter, regulators always face a tough quandary. If emission caps are set too low, they would fail to fully limit pollution; if the caps are set too high, they could constrain or damage their domestic energy sector. Europe’s cap-and-trade carbon credits system was established to address this dilemma.

WHAT ARE CARBON CREDITS? Carbon credits are a tradable certificate that represents the right to emit 1 ton of carbon dioxide (CO2) or the equivalent. By making CO2 emissions a tradeable commodity, "clean" businesses are able to sell their "excess cleanliness" (CO2 emissions below the current global cap) to "dirty" businesses (that are polluting above the cap). Consider a situation whereby Company A needs just 70% of its annual allocated carbon emissions quota while Company B requires 130%. Company A can sell its surplus 30% to Company B, helping the latter meet its credit deficit and offset its emissions excess. In that market, buying carbon credits is as simple as buying any commodity, stock or bond.

The system incentivizes clean energy innovation and environmental conservation. For example, businesses that are unable to comply with the global cap can purchase carbon credits by making finance readily available to renewable energy projects, or perhaps to a reforestation initiative somewhere in the world. These energy efficiency projects replace fossil fuel and industrial processes, thus benefitting the planet.

HOW CARBON CREDITS MARKET WORKS The underlying supply and demand fundamentals of carbon credits are complex, however, the simplified concept is as follows: Participating countries must first agree to adhere to emission caps and are assigned a maximum number of carbon credits. This is the total available supply of credits in the market. If global demand for energy rises, firms can afford to (and must) pay more for carbon credits. If polluters become cleaner, their demand for carbon credits should fall; If polluters pollute even more, their demand for carbon credits should rise. Generally, as the world becomes more developed and energy consumption climbs, carbon credit prices would appreciate over the long-term.

A LONG/SHORT PLAY ON GLOBAL WARMING Investors can gain exposure to that market via the iPath Global Carbon ETN (GRNTF), which invests in ICE-listed carbon futures. Carbon futures essentially behave like any energy commodity with limited supply. If demand for energy and demand for clean air rise simultaneously, the value of carbon credits should as well, which should benefit the ETF. Alternately, if innovative polluters find a groundbreaking technology that does not emit vast quantities of CO2, or if global warming ceases to be a concern around the world, carbon credits could become worthless, which would hurt the ETF.

HIGHER CARBON PRICES AHEAD The carbon markets have put investors through a stomach-churning ride this past decade. Prices halved in the aftermath of the financial crisis before rallying 50% after March 2009 with other financial assets. Subsequent ups and downs ensued over the past 9 years but the most recent melt-up, evidenced by a 365% rally of GRNTF since last summer, is the most dramatic yet and reflects a structural change in the market.

Indeed, the price of carbon emission permits in Europe have more than quadrupled from less than 5 euros a ton since the middle of 2017 to a 10-year high of 20 euros ($23). This is mostly due to the EU’s decision to decrease the supply of permits in an effort to (a) fix a glut in the emissions trading system, and (b) shift its power industry away from using coal and toward cleaner fuels such as natural gas & renewables. Energy consultants at Carbon Tracker go so far as to predict that CO2 prices could double from current levels to 40 euros a metric ton within the next 5 years. They anticipate a carbon credit deficit of about 1.4 billion tons in the power and aviation sectors by that time.

HIGHER GAS PRICES AHEAD As noted earlier, utilities need these carbon credit certificates to cover the greenhouse gas emissions they produce. With the market now counting down to the biggest supply squeeze ever brought on by the European Union Emissions Trading System (EU-ETS), power prices are surging across Europe. That’s because higher emission costs can make it more cost-effective for power generators to use natural gas, which requires only about half the allowances needed to burn dirtier coal. That demand may push up European gas prices, which are already trading at the highest level for the time of the year in at least two decades. In time, this may even trigger political pressure to cap carbon prices, especially if riots were to erupt like the ones in France this month.

World carbon emissions have been increasing by an average of 300 gigatons each year for the last decade, driven primarily by China’s and India’s growing demand for energy. Together, those two countries now account for one-third of world carbon emissions. Last year, China launched its own national carbon market which should expand over time to cover eight of its high-energy intensive sectors, and bring a quarter of the world’s emissions under some kind of trading system. The initial launch applies only to 1,700 power companies and three billion tons of carbon; however, that already surpasses the EU’s Emissions Trading Scheme, which applies to 31 countries and 11,000 heavy emitters spread across multiple sectors, but only manages 1.4 billion tons of carbon.

In the United States, where California already has an established market, at least seven other states are considering the imposition of carbon taxes or plan to join a regional carbon market. Nearby, Canada’s Chamber of Commerce, the country’s largest business group, has just endorsed a carbon tax as the most efficient way to cut greenhouse gas emissions. This is all to say that, unless global warming is proven to be a “hoax” or new technologies are developed to prevent CO2 emissions, carbon prices will likely head higher in the long-term. |

|

|

| We've also summarized the following articles related to this topic in the Energy & Environment section of today's report.

Carbon |

- 9 EU states urge CO2 price floor to meet climate goals

- Around the World, Climate Goals Clash With Reality

- Australia likely to use controversial Kyoto loophole to meet Paris agreement

- Two US electric utilities have promised to go 100% carbon-free—and admit it’s cheaper

- Emmanuel Macron’s carbon tax sparked gilets jaunes protests, but popular climate policy is possible

- Wildfires in Sweden Signal Europe’s Climate Disaster Is Growing

- Harmful Algal Blooms in the Arctic

|

|

|

|

|

|

|

| Change-Driven Theme Updates |

|

|

|

|

| |

| Economics & Trade |

| Iceland Post-Crisis Icelanders Are About 30% Richer Than EU Citizens

According to preliminary data published on Friday by the statistics office in Reykjavik, gross domestic product in Iceland last year was 30 percent above the average in the European Union.

Of the 37 countries ranked, Iceland was fifth from the top. Luxembourg has the highest GDP per capita, at 153 percent above the EU average. Ireland is second, at 81 percent above the average.

Iceland isn’t an EU member, but is part of the European Economic Area. The island bounced back from its 2008 financial meltdown after imposing capital controls, leaving offshore bank creditors in the lurch and restructuring its banks. It also relied on a Nordic welfare model to keep people out of poverty. Its approach to dealing with the crisis earned its policy makers praise from the International Monetary Fund and Nobel laureates including Paul Krugman. Iceland |

| Pakistan Fitch cuts Pakistan credit rating deeper into junk territory

Fitch has cut Pakistan’s debt rating deeper into junk territory as the cash-strapped country grapples with a lethal combination of low reserves, elevated debt repayments and a weakening fiscal position. The rating agency on Friday said it had downgraded Pakistan’s long-term foreign-currency issuer default rating by one notch to B- from B.

The move was in reaction to the country’s rising debt level which is expected to swell due to its weak repayment capacity. At $7.3bn, Pakistan’s foreign currency reserves have dropped to the critical level of around one and a half month of import cover.

Over the next three years, the country’s sovereign debt-service obligations will range between $7bn-$9bn per year, which includes a $1bn Eurobond repayment due in April 2019.

Fitch said that “rupee depreciation, lower oil prices and newly imposed import duties will drive a deceleration in imports, while exports are likely to strengthen gradually.” However, the credit agency added in its statement that this may not be sufficient to re-build reserve buffers sustainably.

This week the global credit rating agency Moody’s also said that it was considering downgrading Pakistan’s external credit rating. FT |

|

|

|

|

| |

| Finance |

| Fintech Robinhood, the start-up upending stock trading, goes after banks with 3% checking and savings accounts

Popular stock trading app Robinhood, which disrupted Wall Street with zero-fee transactions, is taking aim at an even bigger market: banks. The 5-year-old company on Thursday unveiled "Robinhood Checking & Savings," which offers checking and savings accounts with no fees and pays an interest rate roughly 30 times the national average. Customers will earn 3 percent annually on money in either accounts, paid out on a daily basis.

The no-fee model is what you might expect from Robinhood. The Menlo Park, California-based company took Wall Street brokerages by storm by offering stock trading for free. The model put pressure on incumbents like Charles Schwab and TD Ameritrade, which charge $4.95 and $6.95, respectively, for equity trades.

That price war is still intensifying. J.P. Morgan Chase unveiled its own free trading app in August, sending shares of TD Ameritrade and other public online brokers lower that day.

Robinhood is now taking the disruptive no-fee model to checking and savings accounts, a fundamental way retail banks make money. But there's an important distinction between what the start-up is offering and a traditional bank: the Robinhood savings account is SIPC-insured, not FDIC-insured, which means the customer is essentially opening a brokerage account that has different protections. CNBC |

|

|

|

|

| |

| Construction & Real Estate |

| Housing Trouble in Housing? It’s More 1994 Than 2007

Housing market fundamentals in this cycle are nowhere near as risky as they were in the mid-2000s. Real-time data on mortgage applications suggest a milder path. Coincidentally, it looks a lot like 1994.

The economy in 1994 is remembered largely for financial market turmoil brought about by sharp increases in the federal funds rate by the Federal Reserve. The other noteworthy story of the 1994 economy was what happened to the yield curve. Because of the sharp increase in short-term interest rates, the yield curve flattened significantly.

The story in 2018 is similar. While the increase in mortgage rates this year is not as severe as it was in 1994, the housing market is dealing with other headwinds — rising costs from land, labor and materials prices, plus a shortage of inventory after years of building fewer homes than population growth would seem to warrant. An increase of one percentage point in mortgage rates between mid-November 2017 and mid-November 2018 made homes less affordable.

And similarly, this year, we’ve witnessed a flattening, but no inversion, of the yield curve. The spread between two-year and 10-year Treasury rates ended 2017 at 0.52 percentage points, and as 2018 winds down the spread has been falling to close to 0.1 percentage points. B |

|

|

|

|

| |

| Labor, Education & Demographics |

| Population A New Demographic Era Ahead for China

With the globe’s largest GDP (PPP) at $23.12 trillion, China is indisputably a close contender for the title of world’s largest economic superpower along with the United States. But what makes this possible in the first place? The country’s economic clout arguably stems from its human capital: a 1.4 billion-strong population.

Each of China’s 33 distinct regions is home to a population size on par with entire countries. Every region, and especially the massive cities with them, are substantial contributors to the country’s growth and success.

Nevertheless, China’s population may cease to be a strength that contributes to rapid economic growth. In the wake of the infamous one child policy, the country could soon by dealing with the demographic time bomb of a rapidly aging population. By 2050, almost four in ten people in China will be above the age of 60, which will create an added strain on the already declining working-age population.

The good news for China? The country is making moves to combat the challenges ahead, including ambitious plans to build a $1 trillion artificial intelligence industry by 2030 – an attempt to close the impending labor gap. VC |

|

|

|

|

|

| |

| Services |

| Cannabis In the Wild West of pot stocks, U.S. companies create a Green Rush

Four completely different companies combined into a Frankenstein’s monster of a corporation that admits it is breaking federal law every day just by doing business.

On almost all regulated stock exchanges, that beast would not even be considered an option for a stock offering. In the Wild West of pot stocks, though, Tilt Holdings Inc. managed to raise $120 million last week, even after being forced to retract its financial forecast.

That is why the Canadian Securities Exchange has become a destination for cannabis companies, especially a wave of U.S.-based pot companies that grow and sell marijuana despite federal prohibition in their home country. Major U.S. exchanges like the Nasdaq and New York Stock Exchange, as well as the Toronto Stock Exchange — Canada’s most prominent home for share issuances — and sister exchange TSX Venture, will not list companies that break U.S. federal law, but the CSE is more than willing to help them raise money.

As Canadian cannabis companies like Aurora Cannabis Inc. Cronos Group Inc. and Tilray Inc. have managed to list on large U.S. and Canadian exchanges, Carleton said that U.S. companies have taken note and are saying to themselves, “We’re a way better company,” and are seeking their own listing. The CSE is the place for that, and listing there allows U.S. pot companies access to over-the-counter exchanges in the U.S. and potential entry into foreign exchanges in Europe and elsewhere. MW |

| eCommerce California lays out new e-commerce tax requirements

The California Department of Tax and Fee Administration (CDTFA) this week announced new tax requirements for in-state and out-of-state sellers as a response to the U.S. Supreme Court's decision in South Dakota v. Wayfair this summer, according to a press release.

The new law, which goes into effect April 1 and does not apply retroactively, will require out-of-state retailers selling above a threshold of $100,000 or processing more than 200 separate transactions in the state, to collect California use tax.

It's not a new tax, CDTFA Director Nick Maduros clarified in a statement. "Rather, California will now require more out-of-state retailers to collect and remit taxes just as brick-and-mortar retailers have done for decades. With the Supreme Court's decision in Wayfair, California is able to help level the playing field for California businesses." RDive |

| Travel Britons must pay €7 to visit mainland Europe after Brexit

The European commission has confirmed that British citizens will have to pay to visit mainland Europe as soon as the EU’s free movement laws no longer apply. A spokeswoman for Jean-Claude Juncker, the commission’s president, said visitors from post-Brexit Britain would have to fill out an online form and pay €7 (£6) for a visa waiver, which would be valid for three years.

The EU’s European travel information and authorisation scheme (Etias) is aimed at securing Europe’s borders against people-smugglers and terrorists. It will apply from 2020 to all non-EU citizens’ entering the bloc’s border-free Schengen zone and will allow multiple trips within a three-year period.

It is not yet clear exactly what screening criteria will be used, but the details applicants supply, including past criminal convictions, will be matched against Europol databases and their eventual presence on EU and national wanted persons lists or watchlists checked before a visa waiver is granted.

The declaration said both sides wanted to preserve visa-free travel for short-term visits. It implied, however, that visas could be introduced for longer stays. Guardian |

|

|

|

|

| |

| Technology |

| AI Chips China has never had a real chip industry. Making AI chips could change that.

New types of chips are being invented to fully exploit advances in AI, by training and running deep neural networks for tasks such as voice recognition and image processing. China won’t be playing catch-up with these new chips, as it has done with more conventional chips for decades. Instead, its existing strength in AI and its unparalleled access to the quantities of data required to train AI algorithms could give it an edge in designing chips optimized to run them.

China’s chip ambitions have geopolitical implications, too. Advanced chips are key to new weapons systems, better cryptography, and more powerful supercomputers. They are also central to the increasing trade tensions between the US and China. A successful chip industry would make China more economically competitive and independent. To many, in both Washington and Beijing, national strength and security are at stake.

However fast it happens, China’s march to advanced chipmaking is all but unstoppable. No true superpower can afford to outsource technology that is so critical to both its economic growth and its military security. And after decades of playing catch-up, the country is finally seeing opportunities to establish mastery of the field. MIT

|

|

|

|

|

| |

| Commodities |

| Oil Coming changes in marine fuel sulfur limits will affect global oil markets

International regulations limiting sulfur in fuels for ocean-going vessels, set to take effect in January 2020, have implications for vessel operators, refiners, and global oil markets. Stakeholders will respond to these regulations in different ways, increasing uncertainty for crude oil and petroleum product price formation in both the short and long term.

The upcoming 2020 rules apply across multiple countries’ jurisdictions to fuels used in the open ocean, representing the largest portion of the approximately 3.9 million barrel per day global marine fuel market, according to the International Energy Agency.

The International Maritime Organization (IMO), the 171-member state United Nations agency that sets standards for shipping, is set to reduce the maximum amount of sulfur content (by percent weight) in marine fuels used on the open seas from 3.5% to 0.5% by 2020. These regulations are intended to reduce sulfur dioxide, nitrogen oxides, and other pollutants from global ship exhaust.

The 2020 reduction in sulfur limits follows a series of similar reductions in marine fuel sulfur limits, such as those that reduced sulfur content of marine fuels in IMO-designated Emission Control Areas from 1.0% to 0.1% in 2015. Other areas around ports in Europe and parts of China have adopted similar sulfur restrictions. EIA |

|

|

|

|

| |

| Energy & Environment |

| Carbon 9 EU states urge CO2 price floor to meet climate goals

Europe should introduce a CO2 price floor to complement the EU ETS and extend carbon pricing to sectors not covered by the market, a group of nine EU member states said late on Wednesday.

This would send a “clear long-term signal” to investors to incentivise cost-effective greenhouse gas emission reductions, added the group of energy ministry representatives from Denmark, France, Finland, Ireland, Italy, the Netherlands, Portugal, Sweden and the UK.

Although recent reforms to strengthen the ETS were “a step in the right direction”, explicit carbon prices presently only covered 52% of all EU emissions. “In some cases the carbon price can be too low and/or too volatile to trigger effective decarbonisation,” the group added.

The benchmark Dec 18 EUA contract was last seen trading around EUR 20/t but some experts believed it needed to be double that to promote an effective transition to renewables, with the EU goal for cutting emissions standing at 40% on 1990 levels by 2030. Montel |

| Carbon Around the World, Climate Goals Clash With Reality

As negotiators at United Nations climate talks in Poland this week hammer out a rulebook to curb greenhouse-gas emissions, some of the biggest boosters of the 2015 Paris accord are undermining efforts back home to curb global warming.

China is ramping up coal-fired electricity generation despite pledges to cut emissions, according to clean-energy advocates. Canadian provinces are challenging federal carbon-price rules and adopting local policies that go against national emissions goals. And the European Union is bickering over how much carbon dioxide cars should be allowed to emit and subsidies to coal-fired power plants that threaten its climate targets.

Since President Trump’s June 2017 decision to withdraw the U.S. from the Paris accord, China, Canada and the EU have sought to fill the leadership vacuum and uphold the deal to fight climate change.

Their efforts gained urgency in October, when a U.N.-led scientific body warned that the world has 12 years to meaningfully curb global warming or face irreversible environmental changes. High-profile natural disasters this year increased the sense of urgency for many.

“We have all seen that the implications of not getting climate change under control are profound and costly,” EU Climate Action and Energy Commissioner Miguel Arias Cañete said recently. “Business as usual is not an option.” WSJ |

| Carbon Australia likely to use controversial Kyoto loophole to meet Paris agreement

Australia appears likely be allowed to exploit a controversial climate loophole, using carryover carbon credits from the Kyoto protocol to meet its Paris agreement targets. New Zealand has already ruled out using the carryover credits, saying it would discourage other countries from the practice.

Australia’s environment minister, Melissa Price, said Australia would meet its Paris commitment of a 26% to 28% carbon emissions reduction – “equivalent to a halving of emissions per person” – but would not comment on whether the government would use carryover credits from Kyoto to reach that target.

New Zealand’s climate change minister, James Shaw, said this week the practice of claiming credits was not in the spirit of the Paris agreement, and “we would discourage any country from using [it]”. He has previously described the practice as “dodgy accounting” and like “trying to have two meals for the price of one”.

The practice of carryover credits allows countries to count carbon credits from exceeding their targets under the soon-to-be-obsolete Kyoto protocol periods against their Paris commitment for 2030. Guardian |

| Carbon Two US electric utilities have promised to go 100% carbon-free—and admit it’s cheaper

Two US electric utilities recently declared something remarkable: It’s cheaper to tear down their coal plants and build renewable-energy plants than to keep the old boilers running. For the utilities, the goal is now to retire their coal plants and exceed the economy-wide climate targets set in the Paris Agreement: an 80% reduction of carbon emissions from 2005 levels by 2050.

It’s a surprising move by two (primarily) coal-powered utilities in the American West, but get ready for more. Economics, and politics, are fast converging on a consensus. Committing to a 100% carbon-free goal, even before we quite know how to reach it, is good for business.

The first to make the announcement was Xcel Energy, a utility serving 3.6 million people in eight states from Minnesota to New Mexico. On Dec. 4, the company said it would hit an 80% reduction target by 2030, and eliminate all carbon emissions from its power plants by 2050. Two days later, Colorado’s Platte River Power Authority (an Xcel competitor) approved its own goal of 100% carbon-free energy by 2030.

Jason Frisbie, general manager of Platte River Power Authority, said it was just an admission of economic realities, not a political statement. QZ |

| Carbon Emmanuel Macron’s carbon tax sparked gilets jaunes protests, but popular climate policy is possible

The gilets jaunes movement, by its own description, is motivated by broad discontent over shrinking incomes and rising living costs in France. However, the demonstrators in yellow jackets have rallied around one particular government policy: a looming hike in fuel taxes.

Since 2014, domestic excise taxes on energy products have been linked to carbon content, with more carbon-intensive fuels taxed at a higher rate. Tax rates have also been scheduled to increase on an annual basis.

For consumers, this has translated into gradually rising prices for fossil fuels such as petrol, diesel, natural gas, and heating oil. The objective of these rate hikes, according to the French government, is to reduce reliance on imported energy, reduce greenhouse gas emissions and yield tax revenue to cut payroll taxes and stimulate employment.

Unlike other climate policies such as subsidies, carbon taxes make the price tag visible, and that is a big reason for their low popularity. Some commentators have therefore suggested a sequenced approach in which less contentious policies pave the way for gradual introduction of a robust carbon price.

In the long run, the cost of doing nothing will almost certainly outweigh the cost of climate action – but the latter is real and will be allocated unevenly, creating winners and losers. That explains a growing preoccupation with the distribution of climate policy impacts. The idea of a “just transition” is an overriding theme at this year’s climate summit in Poland. It asks us to consider how we can move society to a low-carbon world without leaving anyone behind. Conversation |

| Carbon Wildfires in Sweden Signal Europe’s Climate Disaster Is Growing

Hannele Arvonen, the owner of one of Sweden’s largest lumber yards, is spending the winter months planning for a new and unexpected threat to her business: regular wildfires raging just south of the Arctic Circle.

Her business, Setra Group AB, had a tense summer as firefighters fought back fires raging through Sweden's densely-forested Gaevleborg region during a drought that lasted months. Workers there are still painstakingly trying to recover sellable wood from the charred remains of tree stumps.

The incident is one of dozens highlighting the cost of a rapidly changing climate across Europe. The insurer Munich Re says this year may be on track to break the record for the number of weather-related catastrophe events racked up in 2017, when damages totaled more than 15 billion euros ($17 billion). From German steelmaker Thyssenkrupp AG to British food retailer Greggs Plc, companies are warning that unexpected fluctuations in the weather events are hurting production and sales.

The experiences of these companies show why Europe is leading the international effort to rein in fossil fuel emissions, which steps up pace this week at a round of talks organized by the United Nations in Poland. Envoys from almost 200 nations are working on a rule book to implement the landmark Paris Agreement, where countries rich and poor alike pledged to rein in the greenhouse gases blamed for increasing global temperatures. B |

| Carbon Harmful Algal Blooms in the Arctic

Warming air temperatures and associated major reductions in the Arctic sea ice cover are driving increases in ocean temperature and changes to circulation patterns in the region. These changes are expected to impact the biogeographic boundaries of a range of marine species. For example, it is anticipated that many organisms may migrate northward or become more abundant as air and ocean temperatures continue to warm.

Few pose such significant threats to human and ecosystem health as harmful algal bloom (HAB) species. Data collected over the past decade clearly indicate that multiple toxic HAB species are present in the Arctic food web at dangerous levels, and it is very likely that this problem will persist and perhaps worsen in the future.

Harmful algal blooms, or HABs (commonly called "red tides"), are large accumulations of algae—both microscopic (phytoplankton) and macroscopic (seaweeds)—that affect human, wildlife, and ecosystem health, fisheries (shellfish and fish, both wild and cultured), tourism, and coastal aesthetics.

Marine HAB phenomena affect virtually every coastal country, and take a variety of forms with multiple impacts. Some species produce potent neurotoxins, which can poison humans and wildlife when ingested, causing gastrointestinal distress, neurological problems and death in severe cases. NOAA |

| Energy Blockchain Scientists Say Blockchain ‘Delivering on Energy Promises’

One of the first unbiased, major comprehensive reviews of blockchain has concluded that the technology is “actually delivering on its promises in a number of areas directly related to energy”. Scientists from Heriot-Watt University in Scotland found that blockchain could “further facilitate smart grid applications and decarbonisation of the energy sector”. Writing in the journal Renewable and Sustainable Energy Reviews, they review results from over 140 projects, start-ups and initiatives, covering all areas of blockchains in energy, from transactive community energy models to balancing and trading emission certificates.

Dr Valentin Robu, associate professor at Heriot-Watt University, explains: “Blockchains are often described as holding the promise of enabling a more decentralised, transactive energy system. If we can enable energy generation and use them at a local level, this could allow system operators to reduce expensive network reinforcements, as well as make local communities more energy self-sufficient and resilient to outside shocks in power supply.

“In energy applications, blockchains are often deployed in combination with artificial intelligence techniques such as multi-agent systems and machine learning, which enable smart micro-contracts and local energy exchanges. This can potentially enable building systems and energy service providers to identify consumer energy patterns and develop energy products tailored to the needs of individual consumers.” REW |

| Wind More Than 680 Gigawatts Of New Wind Power To Come Online By 2027

More than 680 gigawatts (GW) of new wind power is expected to come online around the globe in the next decade, according to new research from Wood Mackenzie Power & Renewables.

Wood Mackenzie announced this week that it had upgraded its Global Wind Power Market Outlook Update: Q4 2018 by 2% compared to only a quarter ago, with the majority of the expected growth to occur in the medium-term, boosting annual capacity additions from 2020 to 2023 by an average of 2.7 GW. However, it is the long-term outlook which is most impressive, with Wood Mackenzie analysts forecasting that more than 680 GW worth of new wind power — both onshore and offshore — will be brought online through 2027.

In Europe, Wood Mackenzie expects the maturation of the region’s offshore wind sector will act as a strong driver of growth, while both Japan and South Korea are expected to boast an offshore base of over 2 GW each — not bad, considering neither country has more than 100 megawatts worth of offshore capacity. The burgeoning US offshore wind market also received an upgraded outlook from Wood Mackenzie. Specifically, Wood Mackenzie now expects the US will boast around 10 GW worth of offshore wind by the end of 2027. CT |

|

|

|

|

| |

| Endnote |

| Labor U.S. Jobless Claims Fall to 12-Week Low Amid Tight Labor Market

U.S. filings for unemployment benefits fell to 206,000 in the week ended December 8, below the 226,000 median estimate in Bloomberg’s survey of economists. The decline is consistent with a labor market that remains healthy despite adding fewer jobs than forecast in November. The unemployment rate held last month at the lowest since 1969, and job openings are near a record. The 27,000 drop in claims from the prior week was the largest decline since April 2015, according to the Labor Department. B |

|

|

|

|

|

| |

| |

| The new MRP website has been posting Featured Topic articles daily since its creation in April, included in each is a link to an archived version of that day's DIBs report. There are also over two years' worth of Joe Mac's Market Viewpoints. We've indexed all of this content using the categories you find the DIBs articles filed under, as well as overarching trends such as 'oil' or 'housing.' If it relates to one of our current themes, the content will be marked accordingly. You can use these labels to filter content on the website, and get to what you're interested in faster. There's also a search bar at the top to find what you're looking for under your own terms. Access is only available to MRP clients so you'll need to register on the website to see our articles.

This link will bring you to the registration page, it will ask you for some details and prompt you to select a username and password which you'll use to log into the website in the future. The page is password protected:

Password: 'dibs' |

|

|

| |

| About the DIBs and McAlinden Research Partners

McAlinden Research Partners (MRP) publishes daily and other periodic reports on the economy and the markets.

MRP focuses on identifying change in the global economy and offering an investment thesis whenever an opportunity arises that has not yet been recognized by the market. The DIBs are MRP's compilation of articles and data from multiple sources on subjects reflecting change that have potential investment implications for an industry or group of securities. We share these with our clients who may already have or may be considering exposure in the industries affected. The subjects change daily and constitute an excellent update on featured topics. |

|

|

| The information provided in this Report is not to be reproduced or distributed to any other persons. This report has been prepared solely for informational purposes and is not an offer to buy/sell/endorse or a solicitation of an offer to buy/sell/endorse Interests or any other security or instrument or to participate in any trading or investment strategy. No representation or warranty (express or implied) is made or can be given with respect to the sequence, accuracy, completeness, or timeliness of the information in this Report. Unless otherwise noted, all information is sourced from public data.

McAlinden Research Partners is a division of Catalpa Capital Advisors, LLC (CCA), a Registered Investment Advisor. References to specific securities, asset classes and financial markets discussed herein are for illustrative purposes only and should not be interpreted as recommendations to purchase or sell such securities. CCA, MRP, employees and direct affiliates of the firm may or may not own any of the securities mentioned in the report at the time of publication. |

|

|

|

|

|

|

|

|