| America’s solar industry, which now generates almost 2% of the nation’s electricity, enjoyed a banner year in 2016. Solar even became the nation’s leading source of new electricity generation for a while, until several positive trends that were driving the boom halted last year. But, as the industry navigates these speed bumps, new sources of strength are appearing.

A confluence of factors suddenly appeared last year, creating headwinds for the industry.

Slowing US Market: US solar deployments fell last year, making 2017 the first time in 15 years that there were fewer deployments than in the prior year. A slowdown in distributed solar combined with a decline in the contracted utility-scale pipeline contributed to the downturn. Furthermore, the rush to start new solar projects in 2016, before a federal tax credit was due to expire, pulled ample capacity into 2016 deployment, leaving pipelines depleted for 2017.

Tariffs on Solar Panels: Although congress eventually extended the 30% tax credit through 2019, President Trump’s decision to impose a 30% tariff on imported solar panels added a new complication. Just the idea of a policy change was enough to send buyers scrambling last year, creating bottle necks in the supply chain. Before the tariffs, the US solar industry was expected to have the capacity to power 13.7 million homes nationwide by 2022. Now, that estimate has been revised downward by more than 10%.

Rising module prices: Reversing another long-running trend, solar module prices started to rise last year. This was mostly due to supply constraints from China’s deployment ramp-up, and hoarding in advance of the U.S. decision regarding solar tariffs.

The tariffs are already reshaping the industry and its prospects. Take the example of SunPower, America’s second largest commercial solar-power company, which produces most of its panels overseas. Because the tariffs are costing it as much as $2 million a week, SunPower has decided to merge with SolarWorld Americas, a foreign-owned company that produces panels domestically, that way SunPower can move a bigger share of its production to the US. Similarly, Chinese company JinkoSolar plans to open a factory in Florida later this year.

But, while producing more panels in America will create several hundred jobs, the tariffs could cost tens of thousands of jobs on the installation side of the business, where most of the industry’s jobs are. Although installations are expected to rise, that growth is estimated to be 11% lower than projections before the tariffs. The Solar Energy Industries Association predicts the tariffs could cost as many as 23,000 American jobs this year.

Yet, despite these challenges, the overall outlook remains positive for the US solar industry. Experts are even saying that better times lie ahead, thanks to community solar trends and improving economics.

For one, solar deployments have grown increasingly diversified across the country. While California still represents 39% of installed capacity, that percentage share is forecast to drop into the 20s over the next five years as more installations spread across the US. Florida and Texas, two other large sunny states with massive untapped potential, are poised to surpass current No. 2 North Carolina over the next five years.

Meanwhile, the solar industry just received a big boost from new California legislation that will require solar panels on almost all new homes built in the state after January 1, 2020. SunPower estimates demand for residential solar in the state will increase by about 50% due to the new ruling. More importantly, this mandate offers other states a playbook to follow, which has happened before -- from the 13 states that decided to follow California’s emissions standards to the 28 that followed California’s lead in setting a minimum level of renewables in their electricity mix.

The cost-competitiveness of solar across the country continues to improve, to the point where half of the projects in the pipeline and utility-scale power-purchase agreements are driven by pure economics rather than legal mandates. Groundbreaking solar-plus-storage projects, like the Tucson Electric Power contract awarded to NextEra have brought firm solar power into the realm of affordability.

Favorable land economics are another factor to consider. In some states, such as New Jersey, so-called brownfields are being repurposed into utility-scale solar farms. Brownfields are land which the U.S. Environmental Protection Agency (“EPA”) has declared to be contaminated. These are usually old landfills or industrial parks that might contain pollutants or hazardous materials. As such, Brownfields cannot be used for housing, industrial or commercial buildings. Local governments that own these sites are usually saddled with ongoing maintenance costs, but no redeployment plans. That's about to change.

The National Renewable Energy Laboratory (NREL) estimates that the country’s brownfields cover around 15 million acres. That’s enough land to put up solar energy plants capable of generating 3 million MW, which is equivalent to the current total demand for electricity in the United States. When converted into renewable energy farms, brownfields become brightfields. More than 80,000 brownfields have already been pre-screened by the EPA for possible use as brightfields.

Despite being dealt some obstacles this past year, the solar power industry is still on track to provide 5% of the global electricity mix by the 2030s. That's in a business-as-usual scenario. If the right factors come together, solar power could represent 15% rather than just 5% by that time, according to Wood Mackenzie's MJ Shiao.

Given its brightening outlook, MRP is adding Long Solar to our list of themes. California’s requirement for residential solar panels could be transformational for the US industry. And while President Trump’s solar panel tariffs may put a drag on solar’s competitiveness relative to other sources of power in the near term, every uptick in the price of oil makes solar more attractive, helping to counterbalance that drag.

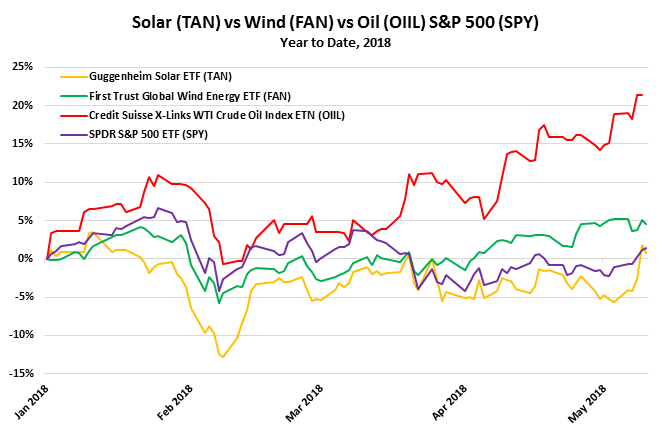

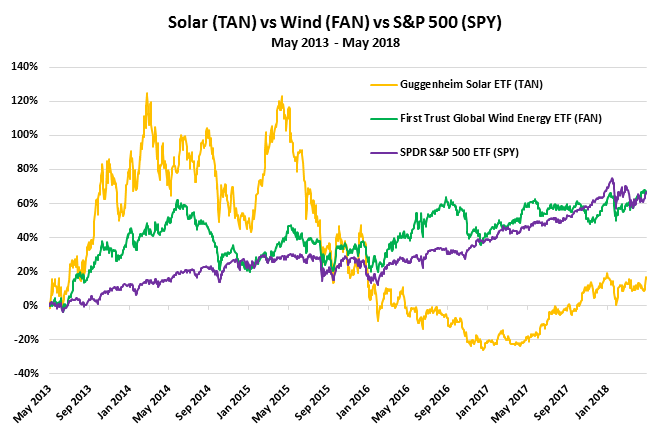

MRP will track the theme via the Guggenheim Solar ETF (TAN). In terms of performance, TAN has risen 42% over the past year, compared to FAN’s 6% gain and the S&P’s 14% gain. But, it is coming from an extremely low base. If you look back over 5 years, TAN has significantly lagged, gaining only 9% versus 65% for FAN and 63% for the S&P.

|