| I. Burgeoning Export Powerhouse

Vietnam, just like China, is still ruled by the Communist Party. And just like its bigger neighbor, Vietnamese leaders have implemented reforms aimed at building a Chinese-style economy: One that is socialist but oriented at fostering private companies. Great efforts have been made to cut back on the number of firms run solely by the state and to aggressively expand Vietnam’s export markets around the world, especially to China and the US. The result is an economy that's been growing on average at a pace of around 6% every year since 2000.

Now, private companies account for almost half of the economy, and Vietnam is the second largest electronics exporter in ASEAN. Investment in electronics is growing so rapidly that high-tech electronics players such as Samsung, LG and Microsoft have set up shop in Vietnam, marking a shift away from China. And while other countries face troubles in their auto industry, the opposite is true of Vietnam. New vehicle sales in Vietnam surged 52.9% year-on-year to 32,308 units during March.

It is no surprise then that Vietnamese manufacturers are seeing monthly improvements in business conditions. As reported by Markit Economics, the headline Nikkei Vietnam Manufacturing PMI came in at 52.0 in May, slightly down from April’s 52.5, but still reflecting an improvement in the Vietnamese manufacturing sector. Both output and buying levels grew at a faster pace, new orders expanded the most so far this year, and overseas sales rose solidly. Growth has now been registered on a monthly basis throughout the past year-and-a-half.

II. Major Trade War Gains: Imports to US Surge 40%, Possible 2.8% Boost to GDP

Meanwhile, the escalation of US-China trade war looks to be a game-changer for Vietnam. To be clear, businesses having been diversifying out of China and into other parts of Asia for years. Labor costs have been the primary driver of that trend: The average wage for a Vietnamese manufacturing worker stood at $3,800 last year, which is about one third of the $10,500 a similar worker in China would receive.

Now though, exporters and multinationals are scrambling to get out of dodge as the world's two biggest economies slap ever higher tariffs on each other’s goods. And as more companies relocate their manufacturing operations out of China to evade tariffs, Vietnam is enjoying a rapid pick up in business.

US imports from Vietnam surged 40% in the first quarter of 2019, compared to the previous year, while imports from China fell almost 14%. At that pace of growth, Vietnam could leap from 12th largest supplier of US imports to 7th largest within a year, overtaking France, India, Italy, Ireland and the UK along the way. Economists at Standard Chartered estimate Vietnam could receive an additional 2.8% GDP growth boost if the Trump administration acts on its threat to slap a 25% tariff on an all Chinese imports.

III. Strong FDI Inflows

Efforts to spur investments are also paying off. Vietnam attracted $19B of foreign direct investment (FDI) in 2018, a 9% increase from the prior year. One fourth of those disbursements came from Japan alone, with South Korea and Singapore rounding out the top three. The manufacturing and processing sector garnered the most interest from foreign investors in the period, accounting for $16.58 billion, or 47% of the registered capital. The real estate sector ranked second with $6.6 billion, or 18.5% and the retail sector came third with $3.67 billion, or 10.3%.

IV. Tax Cuts

Vietnam's parliament is currently considering a proposal that would cut corporate taxes for small and medium sized businesses. Once legislation is formally passed, a clear deadline for implementation will be specified within the legislation itself.

The proposal, submitted by the Ministry of Finance, seeks to reduce the corporate tax from 20% to 17% for “Small Enterprises”. A qualifying business in this category would have an annual revenue that falls between USD $130,000 and $2.2 million and would employ no more than 100 employees. “Micro Enterprises” – those with less than $130,000 in annual revenues and fewer than 10 employees – would have a lower tax rate of 15%. The proposal would also provide a two-year corporate tax holiday to newly started businesses, subject to certain conditions.

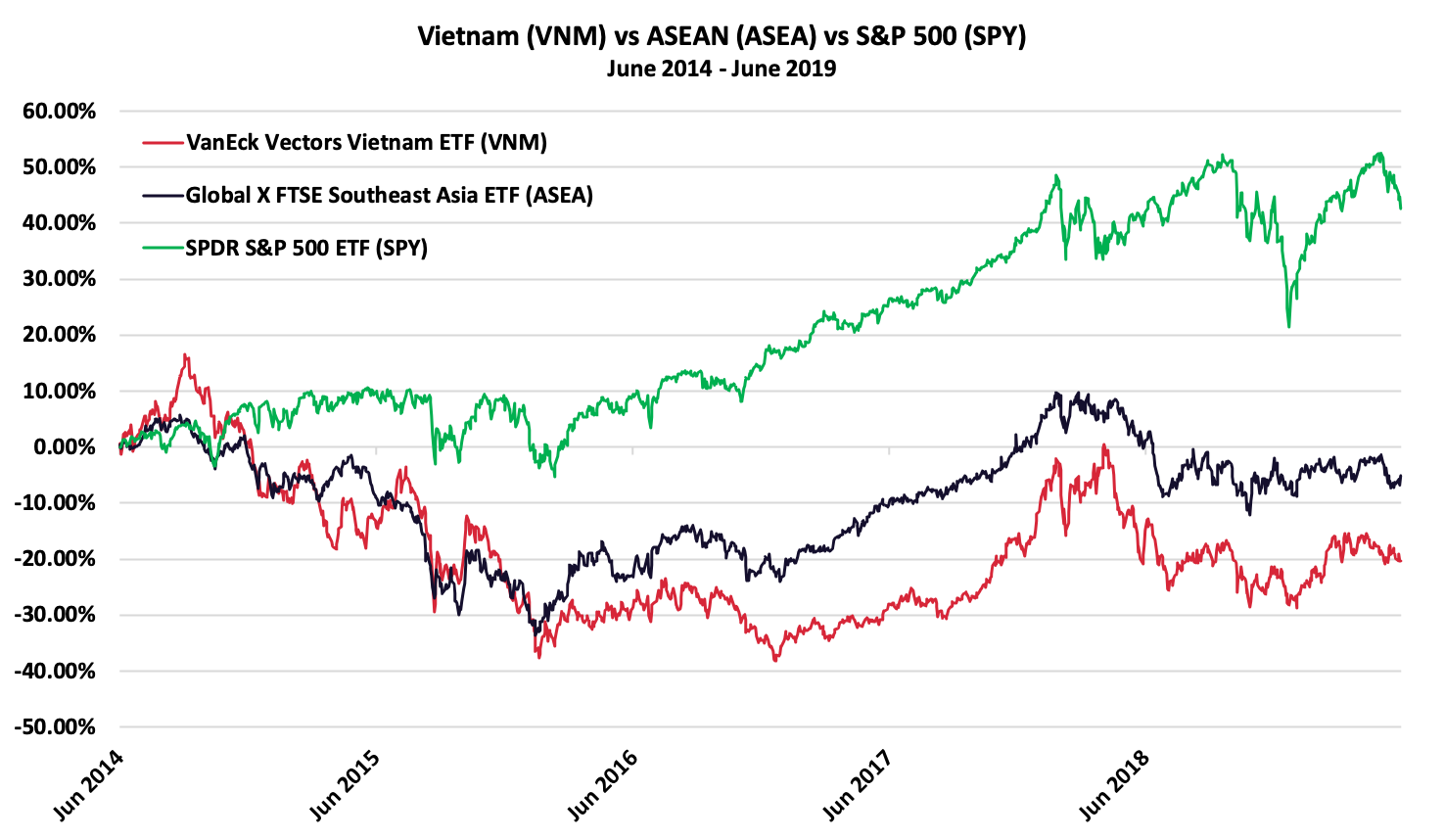

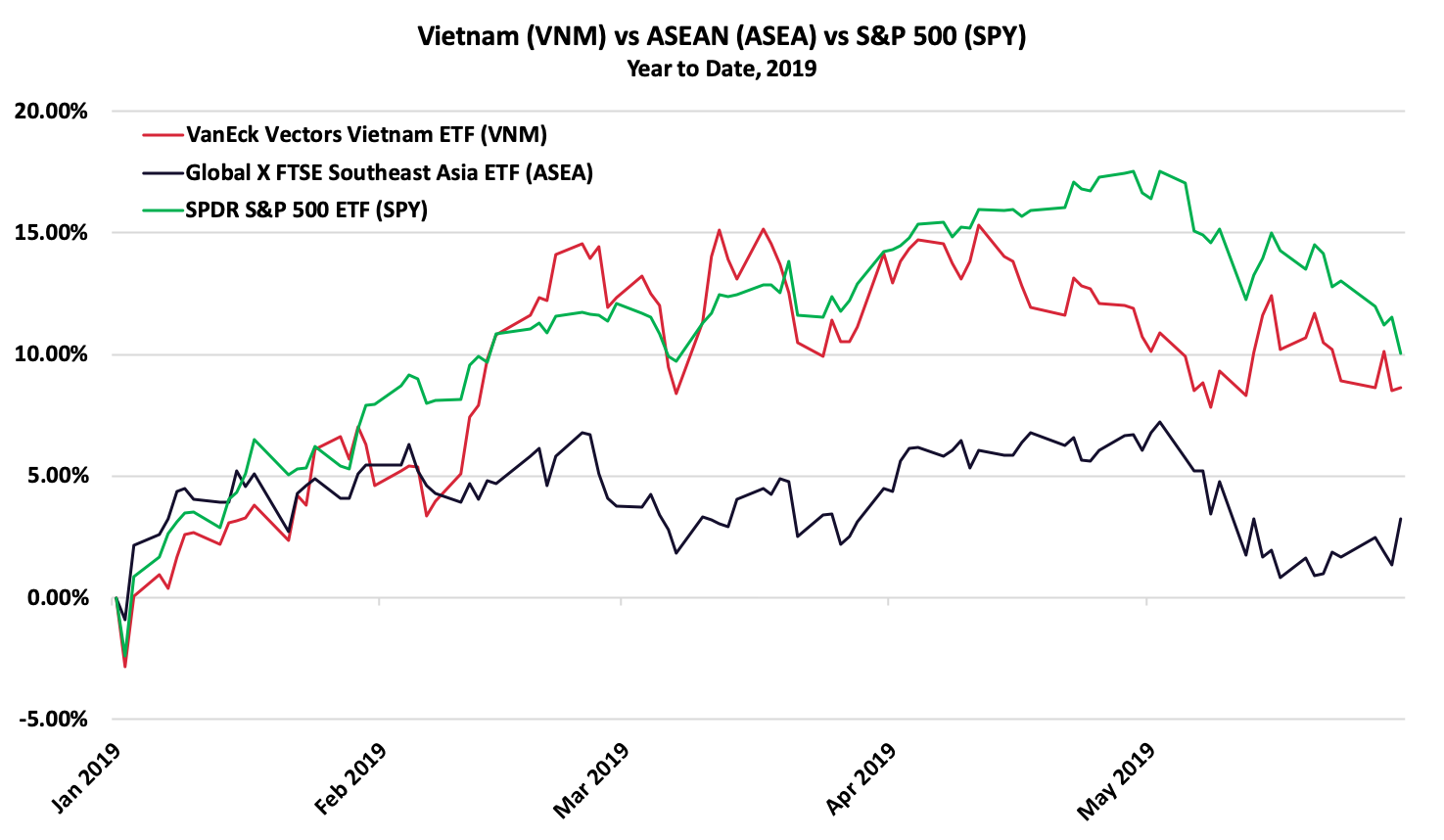

V. Potential MSCI Upgrade to EM for Vietnam Stocks

This month, MSCI will decide whether to upgrade Vietnam to emerging market status. Currently, Vietnam is classified as a frontier market by the major index providers.

Inclusion in the widely-followed MSCI Emerging Market index would be a very positive catalyst for Vietnamese equities seeing that it would attract both capital and new attention to the nation’s stock market. Most private banks and wealth managers are unable to buy or sell Vietnamese equities directly, so the market is still under the radar of the majority of investors.

If Vietnam’s regulators are able to address some technical issues that have held back the promotion in the past, the upgrade to EM status could happen as early as September this year for FTSE and 2020 for MSCI. Most of the issues can be addressed with new regulations, and the Finance Ministry is currently drafting an overhaul for the nation's securities law, the first major amendment since 2010.

Just last month, Fitch upwardly revised its outlook on Vietnam’s credit rating to positive from stable and reaffirmed the country’s BB sovereign debt rating. Vietnam is the second-largest geographic weight in the MSCI Frontier Markets 100 Index. The country's BB credit rating is on par with or, in some cases, better than frontier markets.

Watch Out for Currency Risk …

While the outlook for Vietnamese assets looks positive, currency is one risk factor to consider. Last week, the US Treasury added Vietnam, along with Japan, Malaysia, Singapore and South Korea, to a watchlist for currency manipulation, putting their foreign exchange policies under scrutiny. Countries with a current-account surplus with the U.S. equivalent to 2% of GDP are now eligible for the list, as are countries with a trade surplus of at least $20 billion. Both situations apply to Vietnam which is why the country was added on the watchlist. Being tagged a currency manipulator doesn’t incur immediate penalties, however it can spook the markets.

Another concern is that weakness in the yuan can erode some of Vietnam’s relative strength as a low-cost exporter versus China. As a result, Vietnamese equities tend to be sensitive to movements in the Chinese currency. In 2015, a 5% depreciation of the onshore yuan against the dollar triggered a 15% selloff in Vietnam’s benchmark stock index. But, as noted by one analyst, “when your wages are 1/3 less than China, a few percentage point changes in the yuan doesn’t mean much”. In other words, Vietnam’s cheap labor should help offset the yuan’s fluctuations.

… and for the Impact of African Swine Fever

Vietnam announced on Friday that it has culled 2 million pigs in a bid to curb an outbreak of deadly African swine fever. Vietnam's pork industry is valued at around US$4.0 billion, accounting for nearly 10% of the country's agricultural sector, which is why the government has decided to mobilize its military and police forces to curtail the outbreak.

|