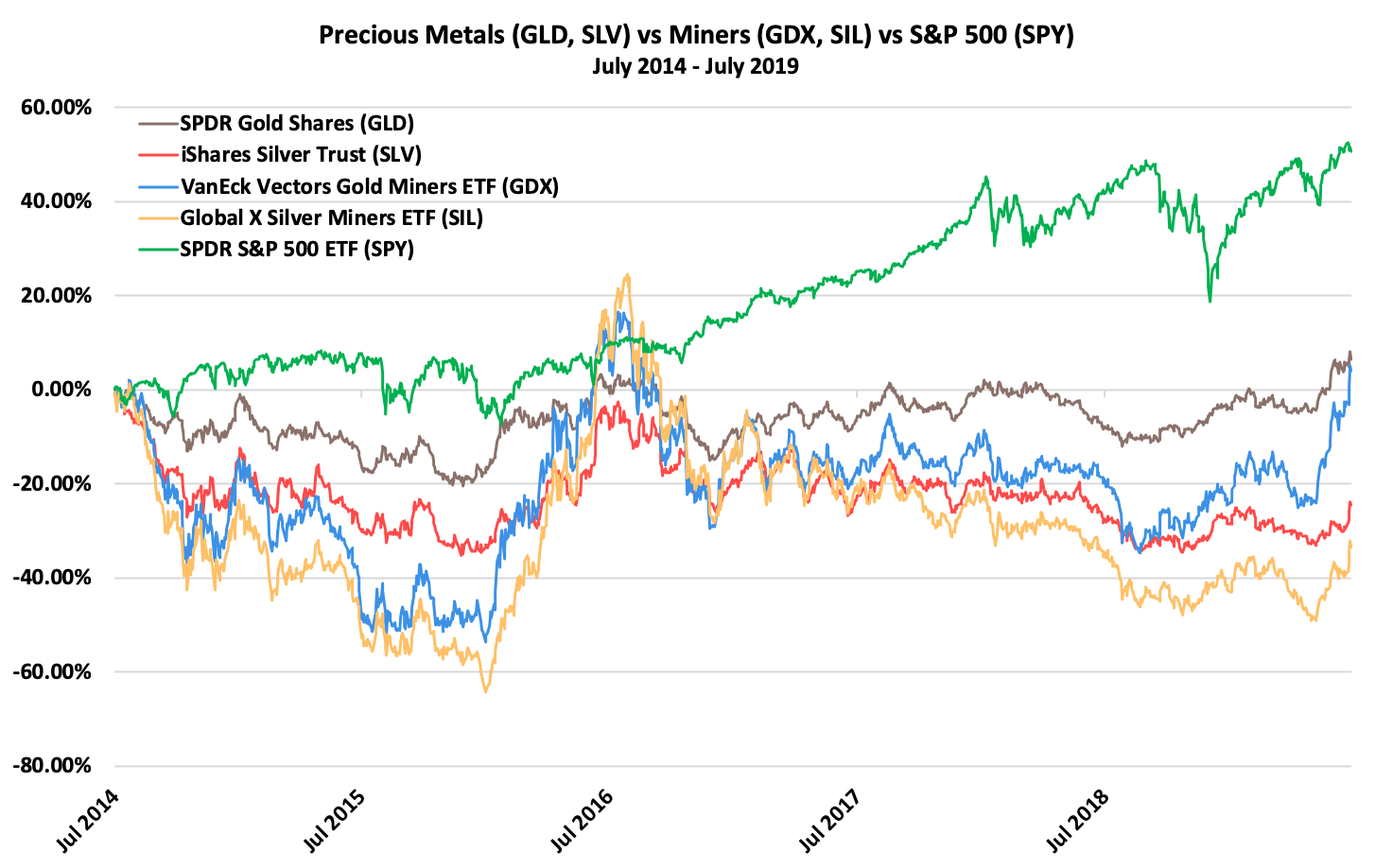

| The precious metals, with the exception of palladium, have badly lagged US equities this decade. But a shift in the global macro landscape has pushed gold and silver prices up this summer. MRP believes we are still at the start of a sustained precious metals rally and that the biggest winners will end up being silver and the silver miners.

Shift in Global Macro Landscape

Investors are witnessing an interesting inflection point right now. The record highs attained by the major US stock indexes this month suggest the equity side of the market is confident that the American economy, with the help of the Federal Reserve, is strong enough to withstand tariff worries and extend the longest-running expansion in history.

The bond market isn’t nearly as confident. Concerns regarding the trajectory of the global economy have triggered a global rally in bonds, causing their yields to sink. Sovereign bond yields in the EU have been negative for some time now, even spilling over into European emerging markets recently, and pushing the total amount of bonds that provide a negative yield to $13 trillion, up from $6tn in October, according to data from Barclays. We’re not quite there on this side of the pond, however, the US 10-year treasury’s current yield of 2.057% is 62 basis points (bps) below where it was at the start of 2019, and near a 2-year low.

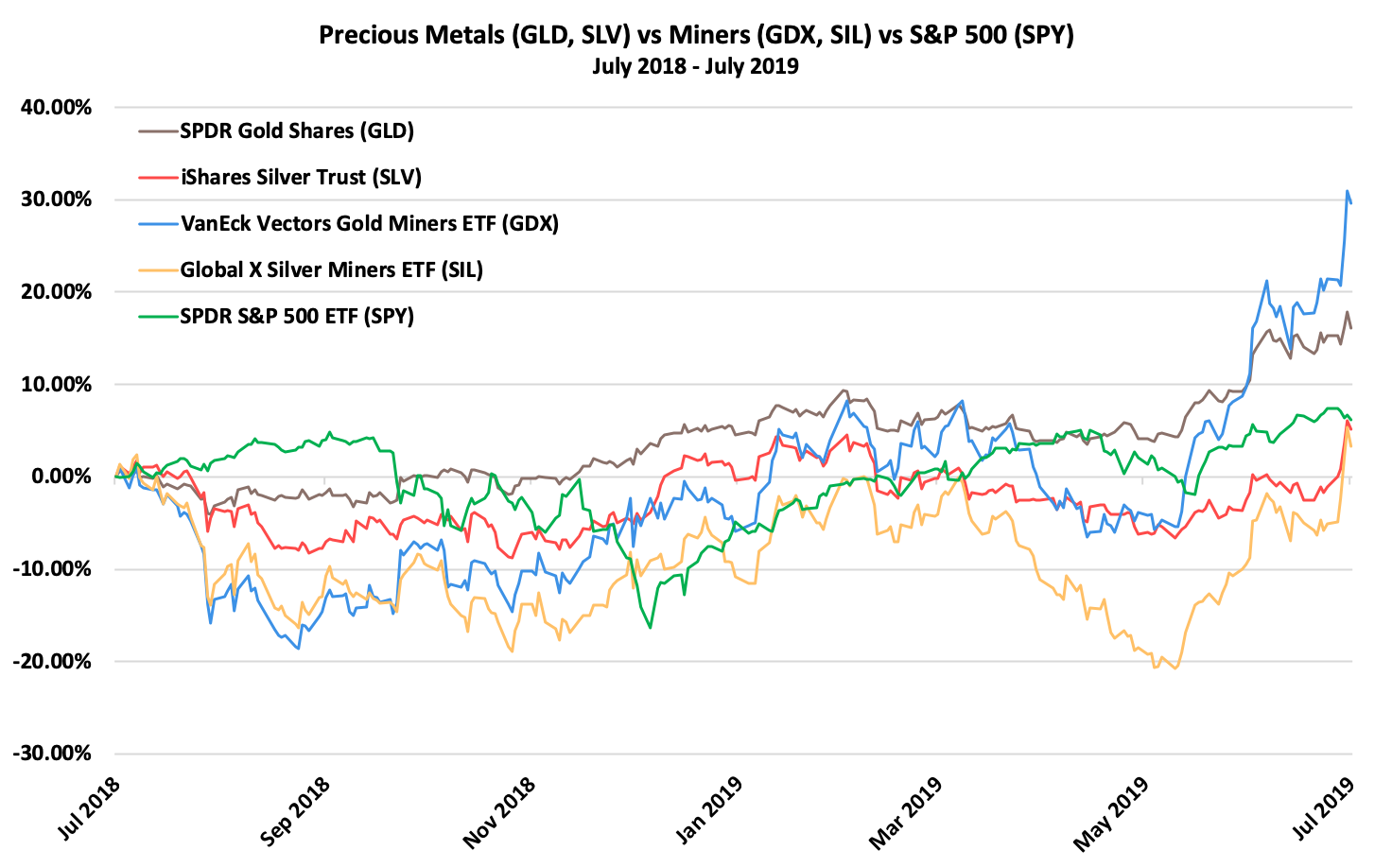

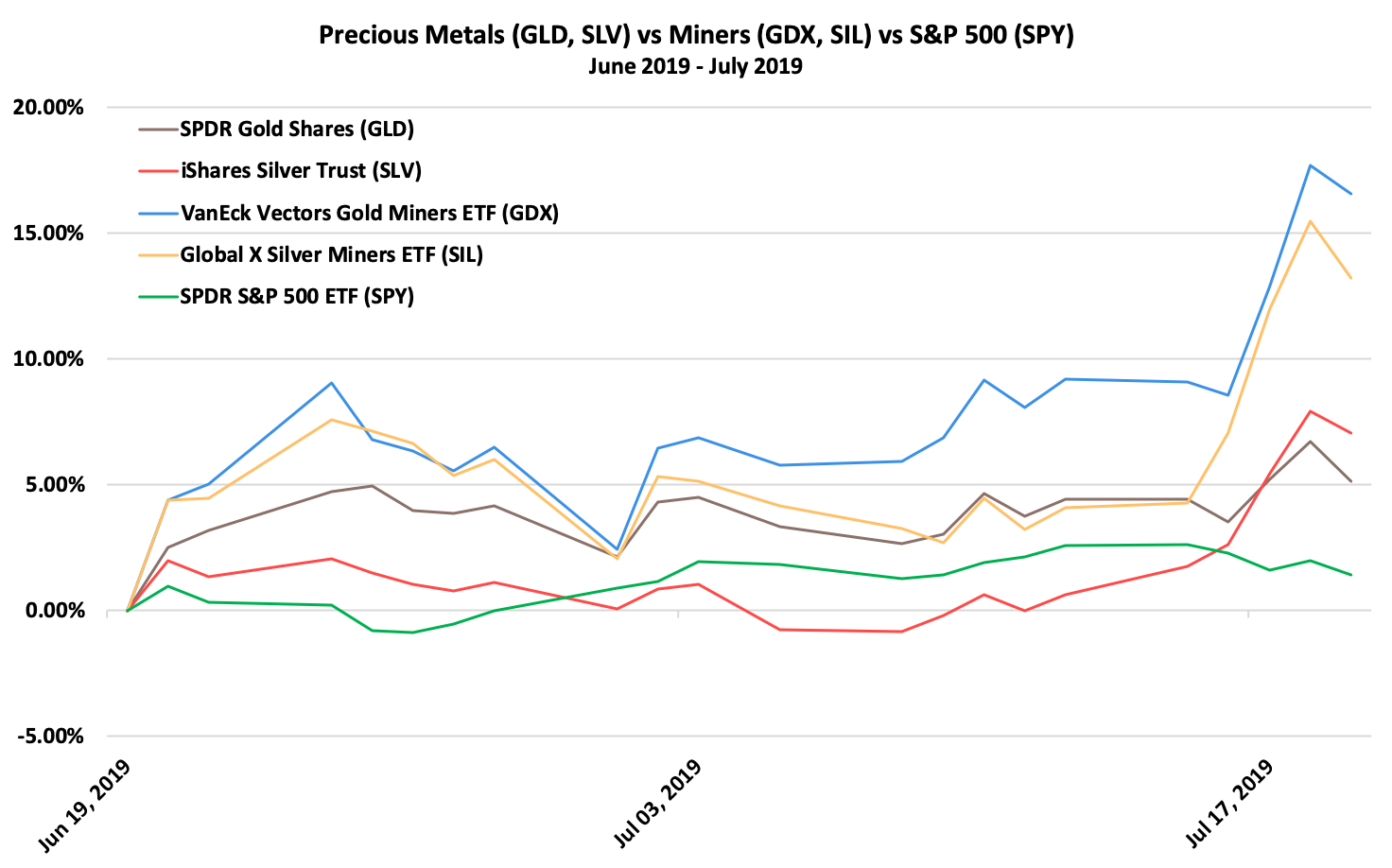

Trade war worries, disquiet about the enormous amount of debt and pension liabilities that will come due in the next few years, and concerns about current equity and bond valuations together have helped the resurgence of precious metals as haven assets. Having languished between $1,350 and $1,375 a troy ounce for five years, gold finally broke through the $1,400 barrier in late June and even managed to briefly trade above $1,450 / oz last week, the highest level in six years. The SPDR Gold Shares ETF (GLD), which mirrors gold prices, is also at mid-2013 highs. Gold’s recent rise has sparked a rally in silver as well.

There’s more of that to come now that the world’s top central banks are about to embark on an easing cycle.

Gold & Silver as Defensive Plays

In a bid to boost their respective economies, the US Federal Reserve is expected to cut interest rates this month, the European Central Bank (ECB) is set for a rate cut as early as September, and the People’s Bank of China (PBOC) stands ready to cut interest rates as a last resort if the trade dispute gets uglier.

Looser central bank policy should push bond yields lower and benefit zero-yielding assets such as gold and silver whose relative attractiveness will rise. Buying gold or silver typically means investors miss out on earning interest on other assets such as bonds and stocks, the so-called “opportunity cost” of buying the precious metal. But tumbling yields would erase that problem. One market observer noted that the correlation between the growing volume of negative-yielding bonds and the rising value of gold was striking.

Moreover, precious metals are increasingly seen by investors as a hedge against slowing global economic growth and, more importantly, against an equity market downturn. Since 2008, the bond market has not acted as a reliable hedge against equity weakness in the way that everyone expected it to. The negative correlation that historically existed between bond and equity prices weakened significantly in the decade following the financial crisis, making bonds a not-so-effective hedge for equities. Accordingly, investors have been turning to gold instead of bonds for protection against a downturn in the US stock market as it continues to make record highs.

In short, the outlook for precious metals is bright whether one is considering matters from a bond market perspective or from an equity market perspective. The same is true if one agrees with Ray Dalio that we are at the start of a paradigm shift that will keep interest rates low and asset prices artificially inflated for an extended period.

Silver’s Time to Shine

Anytime there’s been a flight to haven metals during the past 8 years, gold has been the center of attention and silver has been left behind. Gold closed at $1,425.25 on Friday, so it just has to gain another 30% to reach its September 2011 peak price of $1,852. Silver on the other hand would have to rise nearly 200% from its current price of $16.20 to hit its peak price of $45.30 set in April 2011.

But, the tide is turning. One positive indication is that higher lows are being formed in silver’s price chart. Furthermore, the backdrop for silver prices is extremely favorable right now just based on the Gold/Silver ratio which reached multi-decade highs this summer. The gold/silver ratio is simply the amount of silver it takes to purchase one ounce of gold. It is derived by dividing the current gold price by the price of silver per ounce, and therefore offers a simple measure of how the two metals are performing against each other. So, a ratio of 50:1 (or simply 50) means that, at the current price, it would take 50 ounces of silver to buy one ounce of gold.

Silver typically underperforms gold in the early stages of a precious metals bull market, and the gold/silver ratio got extremely overextended in this cycle, climbing as high as 92 in June, which represents a 26-year high. As of Friday’s market close, the ratio now stands at 88 ($1,425/$16.20). That number, while lower than June’s level, is still significantly above the twenty-year average of 60:1 and a signal that silver is extremely undervalued relative to gold at the moment. This could encourage more investors looking for haven assets to start choosing silver over gold until a reversion towards the mean brings the gold/silver ratio closer to the 60 mark.

In an article on Seeking Alpha, Victor Dergunov notes that “If we look at recent history, we see that every time the gold to silver ratio has reached a level of around 88, it has led to extraordinary rallies in the silver market. We can see this in the early 2000’s, in early 2016, and most notably from 2008 – 2011, when the Fed embarked on its easing and QE programs. During this period silver essentially quintupled going all the way from around $10 to about $50 in roughly 2.5 years.”

One additional factor to consider is that, although silver is a safe-haven asset that tends to perform well when financial conditions become turbulent, it also serves an industrial purpose, unlike gold. Silver is used in electrical applications, medical appliances, electronic devices and myriad other consumer products outside the jewelry category. In fact, industrial demand represents at least 50% of physical silver demand. This means demand for silver should also get a boost from a pick up in industrial activity if the global economy, and the US in particular, avoid going into recession. |