For years, US banks had been concerned about small and nimble fintech upstarts encroaching on their turf. But, Big Tech could end up being the greater threat. Facebook, Amazon, Apple, Uber and Google — companies that already have established relationships with hundreds of millions of consumers — are making forays into banking.

Amazon has reportedly been in talks with J.P. Morgan Chase over creating an online Amazon checking account; Apple in collaboration with Goldman Sachs has expanded into the credit market with Apple Card; Uber announced its push into financial services last month with the launch of Uber Money; and Facebook has just introduced its own digital payment product called Facebook Pay, perhaps as a precursor to banking services.

Now, Google plans to offer Google checking accounts, becoming the latest big tech company to make a move into banking and personal financial services. Google already has offerings in the digital-wallet space, but the potential for an integrated Google bank account could prove appealing to consumers.

Access to Big Data

For incumbent financial services firms like banks, which fear losing their primacy and customers, these types of collaborations are seen as a positive, at least initially. The attraction is that Big Tech will draw younger and more digital-savvy customers who are increasingly looking to handle more of their lives through online tools. Banks can also benefit from Big Tech’s ability to work with huge data sets and turn those into value-add products.

The advantage for Big Tech is equally obvious. Not only do they get to push off the less exciting financial plumbing and compliance tasks to the banks, in doing so, they can avoid the necessity of obtaining a banking license and undergoing the extra regulatory scrutiny that banks must endure. Additionally, working with a traditional bank could help a company like Google overcome consumer skepticism while combating political pushback.

Most importantly, Big Tech companies see financial services as a way to get closer to users and glean valuable data. Checking accounts may be a commoditized product, but they contain a treasure trove of information, including how much money people make, what bills they pay, where they shop, and when.

While these types of joint ventures may draw a broader client base initially, the strategy could backfire on banks if their tech partners, after having obtained the information they wanted, decide to become competitors. Amazon first partnered with sellers on its ecommerce platform but soon started to compete against those same sellers once it was able to glean which products were most profitable to sell.

Having said that, until the deals break apart or regulators in Washington push back on arrangements that give technology companies even more clout, MRP is disposed to view these burgeoning partnerships as a positive for the banks.

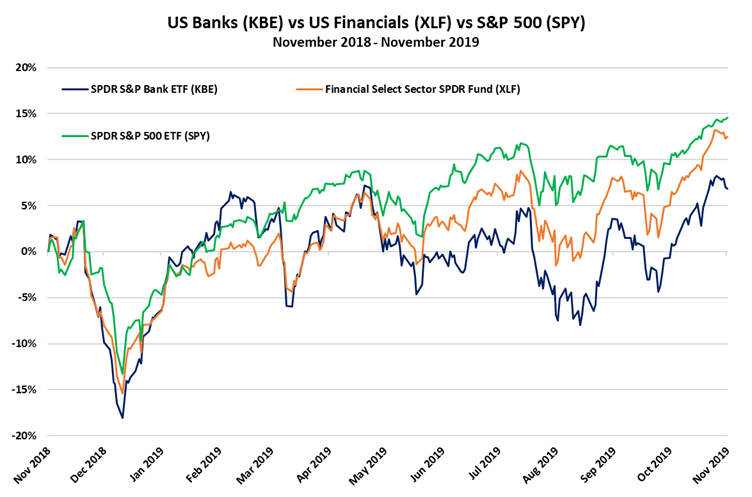

There are other reasons for liking US banks right now.

Improved Macro Economic Backdrop

Just a couple of months ago, the Fed was in the middle of an easing cycle and fears abounded that the US economy was losing steam. Banks thrive in an environment where economic growth is strong and interest rates are rising. So, on both those points, things were looking bad for US banks.

But sentiment has improved since then. Although manufacturing and business investment continue to lag, US economic data is showing strength among households and financial conditions have eased with stocks touching record highs on Wall Street this month.

Testifying before Congress yesterday, Federal Reserve Chairman Jerome Powell expressed optimism about the US economy, saying it is in a “very good place,” with unemployment at near-50-year lows, inflation just under the Fed’s 2% target, and that monetary policy aims to keep the record expansion continuing into its 11th year. Interest rates appear to be on hold for now, and the mere act of pausing the rate hikes is an improvement for banks. If economic growth picks up as trade war headwinds abate, the outlook for banks will be even better.

Steepening Yield Curve

Quantitative analysis has shown the financial sector of the equity market to be more correlated to moves of the Treasury yield curve than most other sectors. Indeed, returns in the energy, financial and material sectors rise the most when the yield curve steepens and fall the most when the curve inverts, as it did in the spring and summer. The yield curved has been steepening lately, which is a positive catalyst for bank stocks.

Cheap Funding

Banks in the United States now get a historic proportion of their funding from deposits, the cheapest form of liability, versus bonds or short-term borrowing. Deposit growth has been accelerating at the largest banks, including deposits into non-interest bearing individual and corporate accounts. The upshot is that some 89% of large US banks’ total liabilities are now deposits, the highest proportion since 1985, and representing a very cheap source of funding for banks to borrow from.

Stronger Fundamentals than International Banks

US financials are in good shape relative to their international counterparts. Our readers may remember that, in addition to writing about US banks this year, we have also highlighted structural issues affecting banks in Canada, China, and Europe. Those threats have not gone away, therefore the recent outperformance of international banks compared to US ones is unlikely to last. |