The UK’s economy has been slowing this year, but that could be about to change. After all, there’s nothing fundamentally wrong with the economy.

The labor market is robust and the unemployment rate, at 3.8%, has not been this low since the 1970s when it hit a record low of 3.4%. In fact, the employment-to-population ratio is at an all-time high. Inflation is below 2%, so the government has room to employ stimulatory measures.

One major drag on GDP has been the marked decline in business investment. Political uncertainty is mostly to blame for that drop. Uncertainty about who will lead the country, about the expected economic regime, and about what sort of relationship the UK will have with the EU have kept investors at bay.

Boris Johnson’s majority win on Thursday removes much of that uncertainty. After capturing 365 of the 650 parliamentary seats in Thursday's vote, his party now has the political firepower to move forward with Brexit. Britain’s withdrawal process will no doubt come with complications that will inconvenience some companies and put others out of business. But it will create opportunity for some other businesses as well.

There are 3 major takeaways from the election results:

- The threat of mass industry nationalizations and higher taxes has dissipated with the labor party’s resounding defeat.

- The political impasse that has paralyzed the country since it voted to leave the European Union in 2016 is finally over. Parliament will convene shortly and begin the legal process to approve Johnson’s withdrawal agreement. By January 31, 2020, the UK will be out of the European Union.

- The fiscal brakes are coming off. Diverging from Margaret Thatcher’s brand of fiscal conservatism, Boris Johnson has pledged £100 billion ($128 billion) of investment into capital projects and he means to finance those with extra borrowing over the next five years. That stimulatory shot of spending should help rekindle economic growth.

There is still plenty to sort out in the year ahead. For example, the Prime Minister has pledged to "get Brexit done" by January 31, but can he actually ink a trade deal with the EU before the end of the transition period in December 2020? Skeptics allude to the fact that Johnson, an erstwhile hard-Brexiter, has promised not to extend the transition period beyond the end of next year, which could cause Britain to crash out of the EU market without a deal at the end of 2020.

The rebuttal to those concerns is that Johnson has until July 1 to ask the EU for a trade talk extension. In the meantime, the UK will be free after January 31 to strike free trade deals with other nations that do not already have a trade agreement with the EU, such as the United States. Getting even a partial deal signed could give Johnson some bargaining power with the EU.

Furthermore, there is more at stake than just a trade deal, therefore it is very much in Johnson’s interest to get a deal done. As pointed out in this Washington Post article, one consequential result of the election is the landslide victory in Scotland of the Scottish National Party (SNP) which opposes Brexit and favors independence. SNP leaders are already calling for a new referendum on Scottish independence. The latest poll on that issue indicates that a majority of Scots (55%) would prefer to be part of the UK, but they may change their minds if Brexit is bungled.

Similarly, the allegiance of Northern Ireland and even Wales to the United Kingdom may also crumble if Brexit is poorly managed. No occupant of 10 Downey Street wants the legacy of being the person who contributed the most to the breakup of the United Kingdom, not even Boris Johnson. To preserve the union with Scotland and Northern Ireland, Johnson may adopt a more centrist course when negotiating with the EU.

So while we do not yet know the trade terms to be faced by British exporters in the future, there are good reasons to be optimistic about a “soft Brexit” happening. In that scenario, the UK and the European bloc would be closely aligned in terms of trading arrangements, avoiding the disruptions to trade and supply chains that a no-deal Brexit would trigger.

Impact on UK Economy & Markets

It is too early to tell how the UK will fare long-term following its exit from the EU. But we do know that breaking the political deadlock begins to remove some of the crippling uncertainty that has weighed on the country’s economy and stock market.

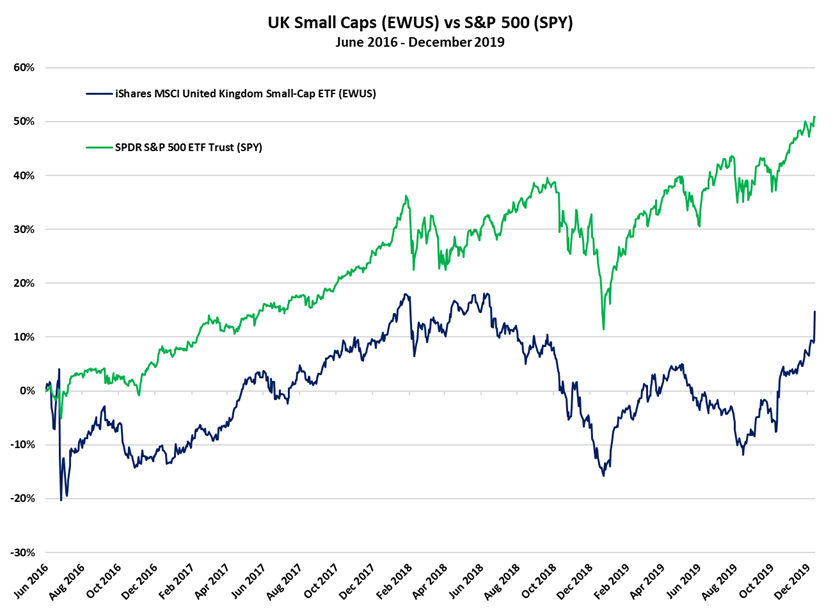

Global fund managers have been underweight UK equities since the Brexit referendum in June 2016. Bloomberg reports that was still the case going into last Thursday’s vote.

To investors that remain on the fence, we would say that the improved visibility combined with the prospect of government stimulus are positive catalysts that should help resurrect business investment, a key GDP growth driver that’s been anemic for a couple of years. That in turn will boost the economy and draw more inflows into sterling assets. |