While the Covid-19 pandemic and low oil prices have dented global electric vehicle (EV) sales this year, penetration rates are improving in some large auto markets like Western Europe and China, helped along by regulation.

The European Commission, for instance, has carved out funds from its €750 billion green recovery plan to help boost EV sales. This trend is reinforced at the national level, with Germany, France and other members of the block handing out cash for electric cars and their infrastructure as part of a huge stimulus splurge. Over in China, EV sales are expected to be significantly higher in the second half of 2020 than the corresponding period in 2019. China is also still sticking to its goal of attaining 25% market share for electric and fuel cell vehicles by 2025.

BloombergNEF (BNEF) estimates that global EV sales will fall by 19% in 2020 — to 1.7 million from last year’s 2.1M — before rising again in 2021 as battery prices fall, energy density improves, more charging infrastructure is built, and sales spread to new markets. The research group anticipates worldwide electric car sales will reach 8.5M by 2025, then go on to surpass 26 million by 2030. By 2040, over half of all passenger vehicles sold are expected to be electric.

Bright Outlook for Battery Demand

Lower battery prices are key to getting more consumers to shift from autos with internal combustion engines to EVs. That’s because batteries account for 25% to 40% of total manufacturing costs for a standard electric vehicle. That is set to drop to 20% or less in the next few years, driven in part by competitive pressures and in part by the introduction of new cell chemistries and innovation in manufacturing equipment & techniques.

Battery prices, which were above $1,100 per kilowatt-hour in 2010, have fallen 87% to $156/kWh, on a volume-weighted average basis. BNEF sees battery pack prices falling below $100/kWh by 2024 and approaching $61/kWh by 2030.

Meanwhile, the outlook for battery demand has never been more positive. Forecasts published on Statista show global demand for batteries increasing nearly ten-fold this decade, going from 282 GWh in 2020, to 970 GWh by 2025, and to 2,600 GWh by 2030. This growth will be driven by consumer electronics, stationary energy storage, and the electrification of transportation.

In fact, some of that demand has been fast-tracked by the increased number of electric two-wheelers (e-scooters, e-bikes, mopeds) in cities around the world, as people try to avoid public transportation in the COVID-19 era.

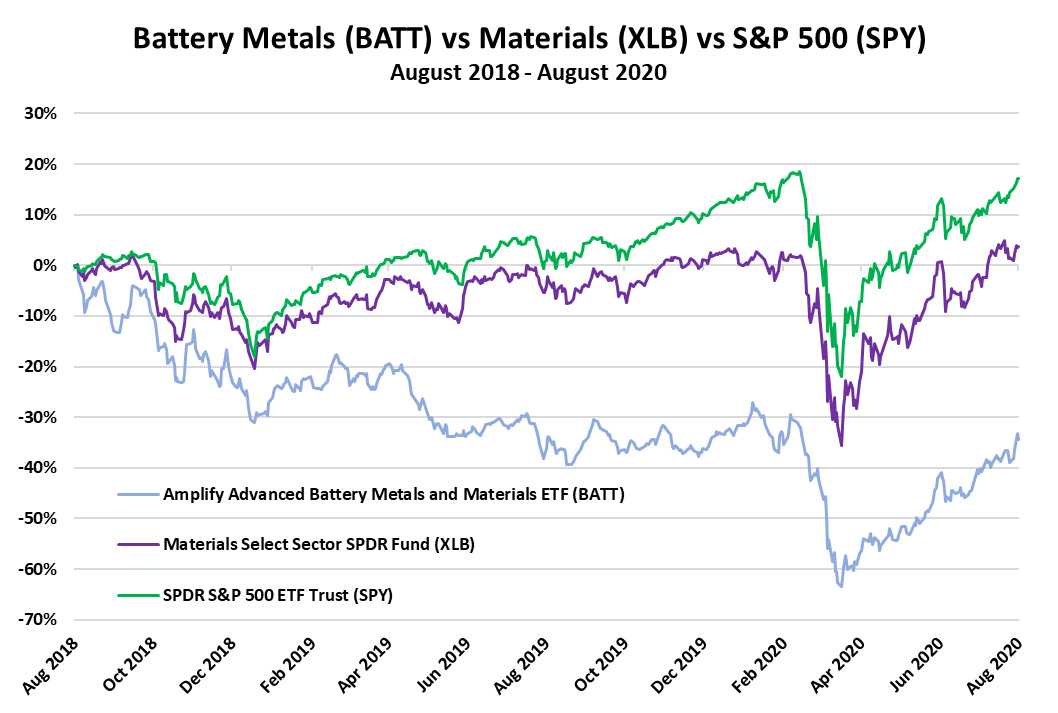

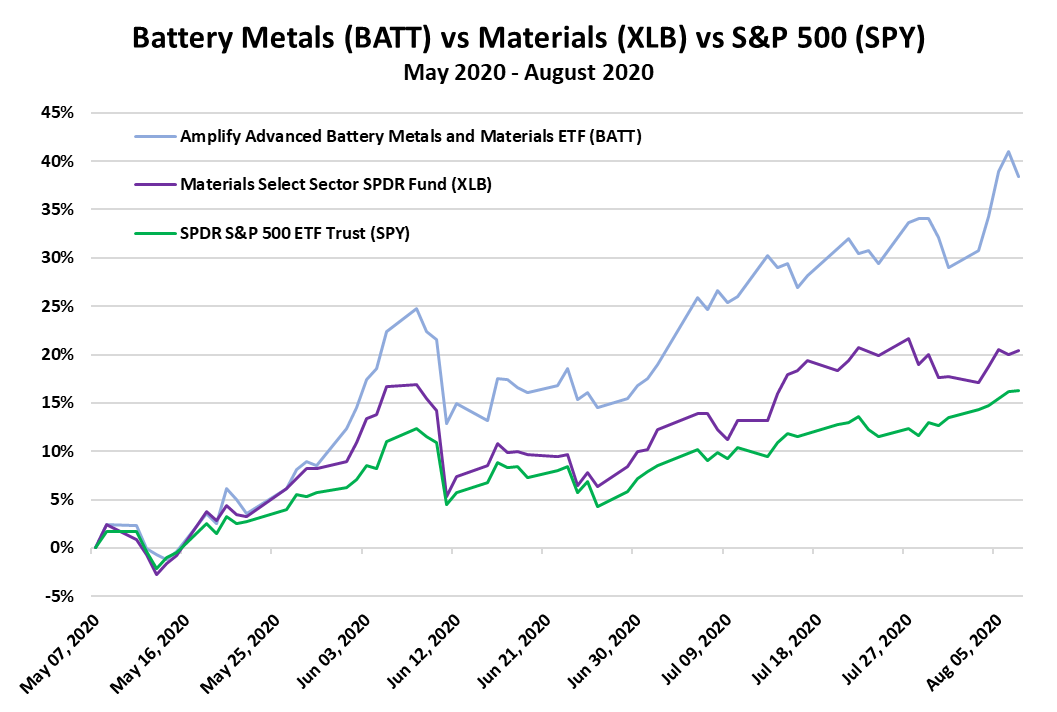

Battery Metals Are Entering a New Upcycle

All of this is very bullish for battery metals. As noted above, battery production can represent up to 40% of the cost of an electric car, with raw materials (including metals like lithium, cobalt, graphite, nickel etc.) comprising the bulk of that cost.

The past few years have been especially volatile for battery metals. We saw the price of key materials like lithium and cobalt soar to astronomical levels in 2016 & 2017 only to come crashing down in the succeeding two years. To put it simply, scarcity concerns coupled with the auto industry’s scramble to secure adequate supplies drove the prices of these metals so high that battery manufacturers had to search for alternatives or reformulate their EV battery chemistries to reduce the content of those premium metals. Producers, overly-optimistic about near-term demand, flooded the market with too much supply. Eventually, prices collpased.

When it looked like a recovery was in the cards for 2020, the pandemic sent prices crashing again as automobile production and renewable energy deployments came to a halt in the first half of 2020. To cap things off, battery manufacturers were forced to delay production due to a shortage of labor, raw materials, and logistic issues.

New EV Battery Metal Index

Going forward, it will be a lot easier for investors, manufacturers, and suppliers alike to monitor the industry’s raw material supply chain and avoid the level of volatility experienced these past years. This is thanks to a new index, launched a few months ago, that’s designed to improve transparency.

The MINING.COM EV Metal Index was built specifically to track the value of battery metals in newly sold EVs around the world — apparently the first time that any such type of measurement (open to the public) has taken place. Two sets of data are used to create this index:

- Prices paid for the mined minerals as they entered into the global battery supply chain

- The sales-weighted volume of raw materials in EV batteries

According to CleanTechnica, the index shows an industry that’s in better shape than last year’s falling prices and bleak news stories seemed to imply.

Things will only improve now that factories are coming back online, and production of electronics, automobiles and energy storage are rebounding.

Also consider that there are over 100 battery megafactories planned around the world. BNEF notes that manufacturers have announced plans to add 1,769TWh of annual capacity by 2025. In order to keep those all factories powering their growing numbers of electric cars, increasing amounts of lithium, graphite, cobalt, and nickel will be needed. Companies involved in the procurement of those metals will benefit immensely. Battery Metals Demand & Supply Forecasts

In our May 19 report on lithium, MRP argued that suppressed prices and weakened demand for lithium had compelled financially-strapped miners to suspend development projects, potentially paving the way for a deficit in the future. With the curtailment of new and existing supply, the market is beginning to rebalance as excess inventory gets used up. Meanwhile, lithium demand is forecast to triple from 300,000 tonnes to 940 000 tonnes over the next five years. Citigroup analysts now expect battery-grade lithium prices to surge by about 42% from current levels thanks to “rising conviction” on EV demand and accelerating rationalization in supply.

Cobalt also faces supply constraints due to the pandemic and the shutdown of Glencore Plc’s Mutanda copper and cobalt mine last year. Mutanda provided about one fifth of the world’s cobalt production in 2018. Demand for cobalt is expected to increase by 55% over the next five years.

Demand for battery-grade nickel is projected to grow by over 150% over the same five years, climbing from 400 tonnes to 150,000 tonnes. One analyst from BNEF posits that there may be a significant deficit as early as 2023 when nickel prices start to recover.

|