Saudi Arabia, continually reaping the benefits of persistently high energy prices throughout 2022, is utilizing revenues from the oil trade to expand other sectors of their economy as part of the Vision 2030 project – a major investment initiative meant to attract new business to the country, diversify away from oil, ease social restrictions, and establish a legacy for the Crown Prince and Prime Minister of Saudi Arabia, Mohammed bin Salman (MBS). MRP has been following the implementation of Vision 2030 since 2018, which was temporarily hamstrung by COVID-19 and low energy prices that were nowhere near what the country needed to address its budget.

However, over the last couple of years, the breakeven price for the Kingdom to balance their budget has fallen significantly, declining from $106.30 to $79.18 between 2014-2022, and now even further to just $69.02 for 2023. International benchmark Brent crude is currently trading north of $92.00 per barrel, about 33% greater than the minimum price level Saudi Arabia will need to address fiscal needs. Per Zawya, Saudi Arabia registered a budget surplus of nearly 78 billion riyals ($21 billion) in the second quarter of 2022, an almost 50% rise from a year earlier.

As MRP noted in August, International Monetary Fund (IMF) data projects Middle Eastern nations will land a $1.3 trillion windfall from extra oil revenues over the next four years. GCC nations – Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, and Oman – will experience an especially significant gain from surging energy revenues in the near-term, collectively increasing economic growth by 6.4% this year, from 2.7% growth last year.

When these revenues eventually begin to recede, research shows Saudi Arabia’s economy will be much more durable and less vulnerable to the swings in commodity markets. Measured by total gross domestic product (GDP), the kingdom’s economy is estimated to become 60% more resilient to oil price shocks by 2030, according to a new study by the King Abdullah Petroleum Studies and Research Center (KAPSARC).

Saudi Arabia, the largest economy within the GCC, is growing particularly quickly, on track for its fastest rate of economic expansion in nearly a decade. The IMF forecasted Saudi Arabia’s GDP to increase by 7.6% this year, among the strongest rates of growth in the world, helping the Kingdom make up ground from just two years ago when its GDP shrank by -3.4% during the height initial stages of the COVID-19 pandemic. There is no better time than now for Saudi Arabia to seize the initiative and aggressively pursue a long-term diversification of its economy.

News broke this week that Saudi Arabia plans to launch a second national airline and is seeking up to 80 new planes from Airbus and Boeing. Bloomberg reports that the potential purchase, funded by the kingdom’s Public Investment Fund (PIF), is seeking an initial order of 40 planes and purchase options for a similar number. Per Skift, 40 A350 jets from Europe’s Airbus would be equivalent to a price tag of about $12 billion.

Transportation in and out of the Saudi capital, Riyadh, will be critical in making it a global hub for business. That goes not only for the transportation of people, but the transport of goods and services as well. In that vein, MBS just announced an initiative to attract investments in supply chains to and from the kingdom, with an aim of raising 40 billion riyals ($10.64 billion). That raise is part of a larger goal of investing over 500 billion riyals ($133 billion) into infrastructure, including airports and seaports, by the end of the decade. Middle East Monitor notes that Saudi Arabia is already the most-visited country in the Arab world, according to figures released by the World Tourism Organization (WTO), with over 18 million tourists visiting the kingdom thus far in 2022, surpassing the United Arab Emirates’ (UAE) volume of tourists at 14.8 million.

Perhaps the largest project Saudi Arabia is focusing on is Neom, a new developmental region along the northwestern coast of the Arab peninsula, built on an expanse of land the size of Belgium. The key subproject of Neom is “The Line”; two parallel skyscrapers that cut through the Arabian desert for 170 kilometers, meant to accommodate 9 million people on a footprint of just 34 square kilometers. Two additional pieces of Neom will be Trojena, a mountain destination meant to offer year-round outdoor skiing and adventure sports, as well as Oxagon, another futuristic residential area in Neom that will function as a port city in the Red Sea.

CNBC notes that the budget for Neom is currently pegged at $500 billion, a significant portion of the total outlays for real estate and infrastructure projects in Saudi Arabia’s National Transformation Plan, now worth $1.1 trillion.

This project was long met with skepticism about its feasibility or whether it would ever even get off the ground following several setbacks throughout the past half decade. Over the last week, however, the ground has been broken and excavation work finally begun for Neom. While there is much more work to be done before anyone can assume the scale of this project is truly manageable, Saudi Arabia undoubtedly finds itself in a stronger geopolitical and financial position today than few would have imagined possible just a few years ago. The ambition of the young crown prince and his government is illustrative of great potential ahead for the kingdom.

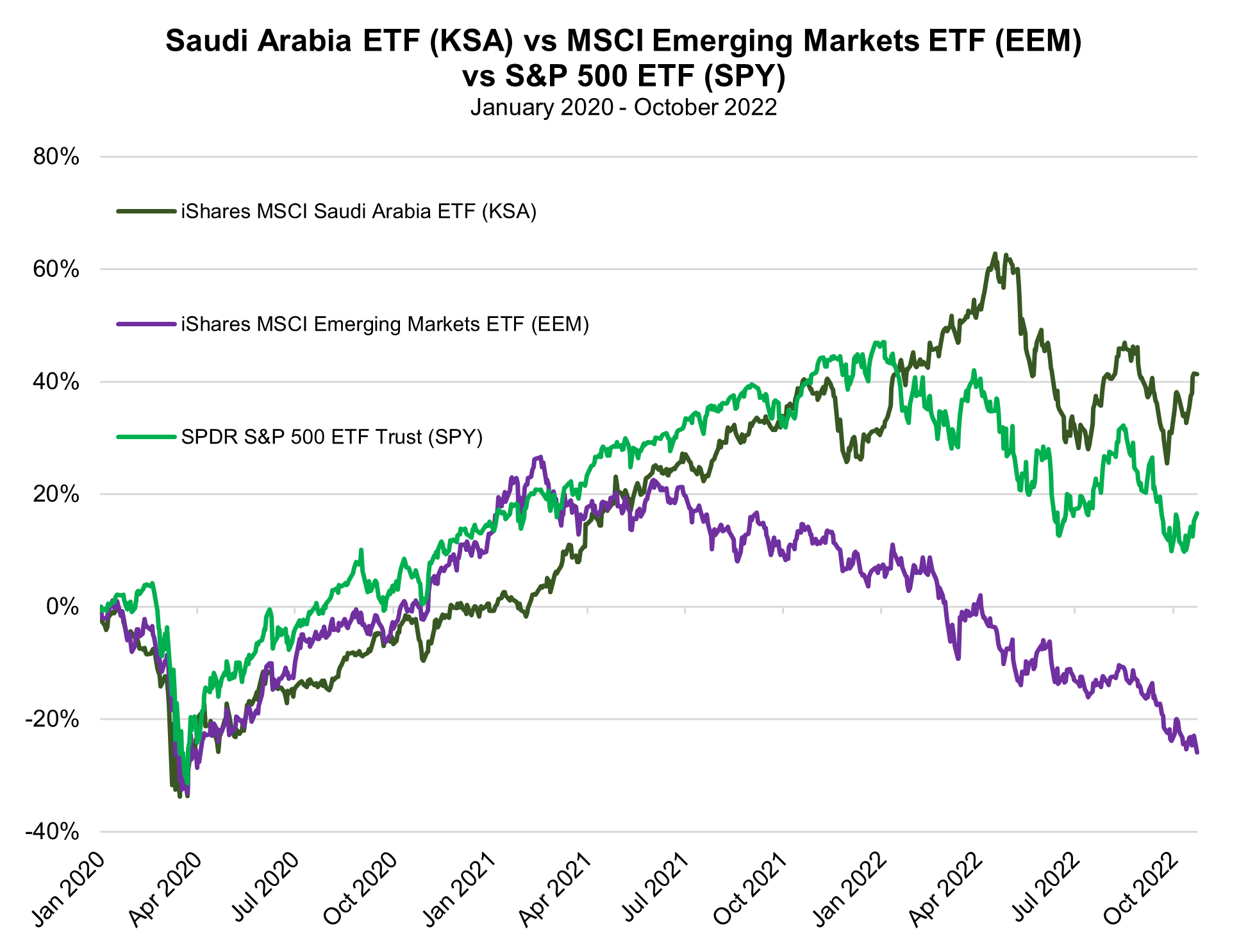

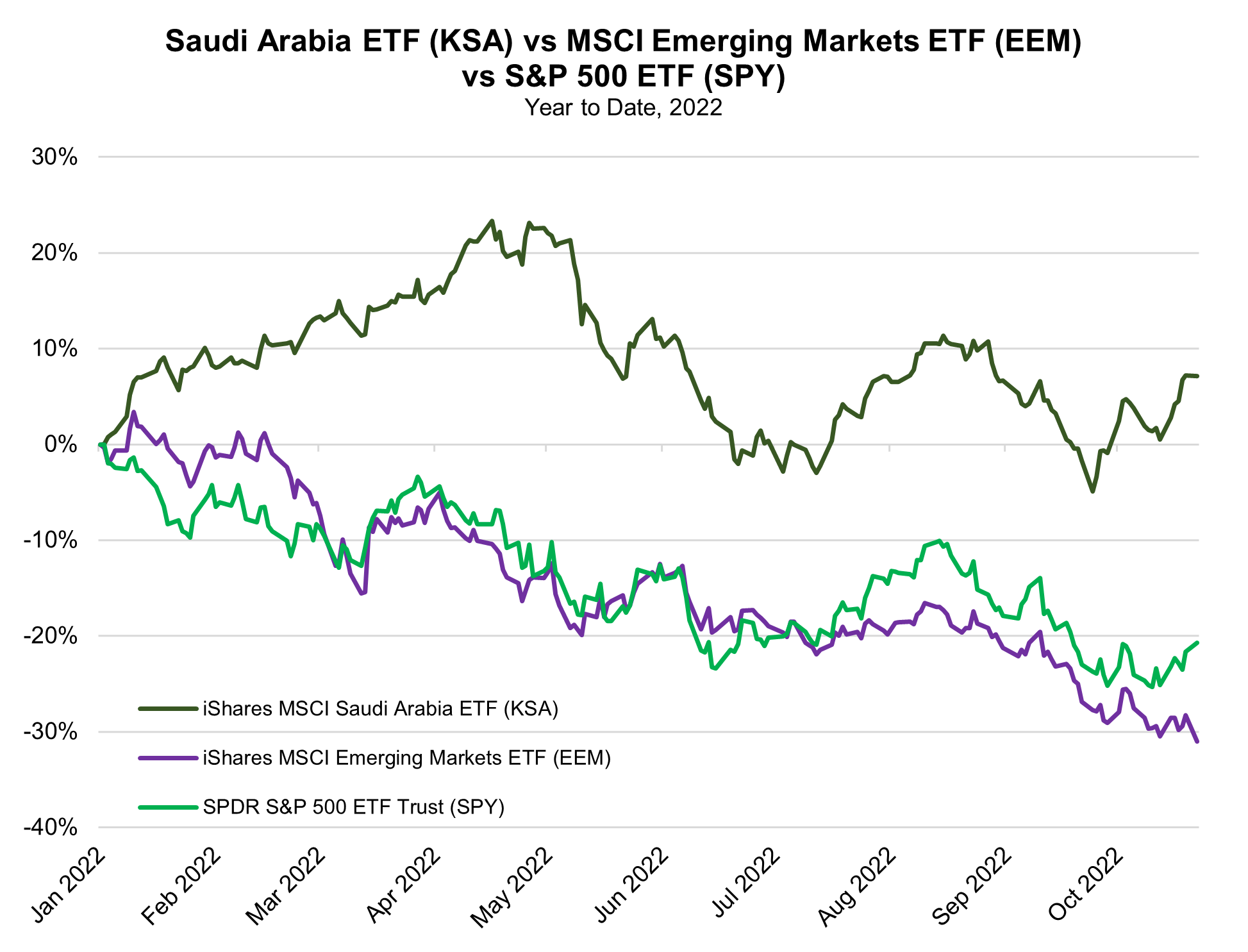

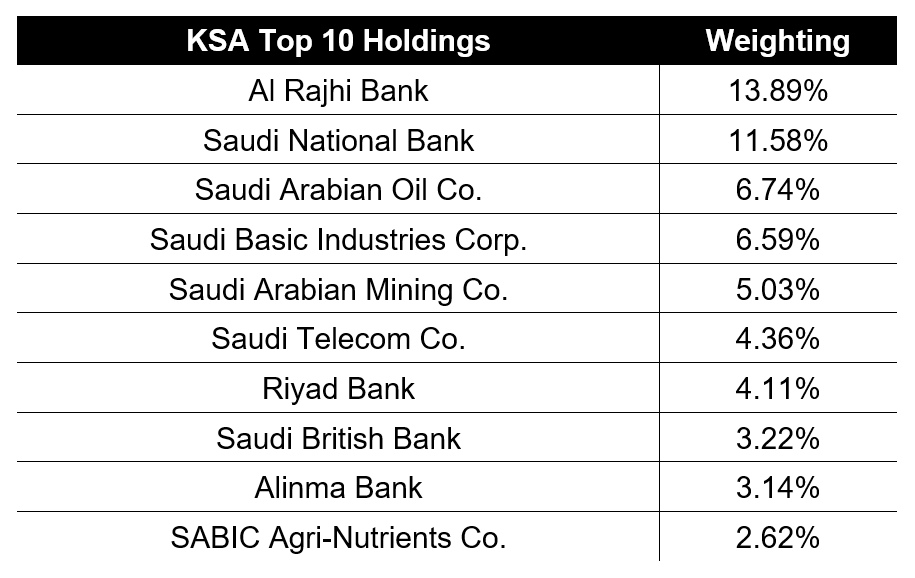

Investors can gain exposure to the transformation of the largest gulf economy via the iShares MSCI Saudi Arabia ETF (KSA) which has gained 7% year-to-date, much better than the S&P 500’s decline of -21%, and further outperforming the iShares MSCI Emerging Markets ETF’s (EEM) return of -31% over the same period. |