An equities rally at the start of the year hit a brick wall in February. That was largely due to anxiety regarding the effectiveness of the Fed’s ongoing tightening, as well as an uncertain path forward that could herald a hawkish resurgence. Though the softening of inflation appears to be more gradual than some had expected, the decline in monetary aggregates and balance sheet assets at the Fed is quietly showing signs of more significant progress. We’ve yet to see the real “pain” that Fed Chair Powell promised last year, but a rise in real rates and deteriorating industrial activity across the economy may be signaling turbulence ahead. Additionally, inversions in the yield curve remain a pressing concern.

Fed Policy Speculation Stifled Stocks in February

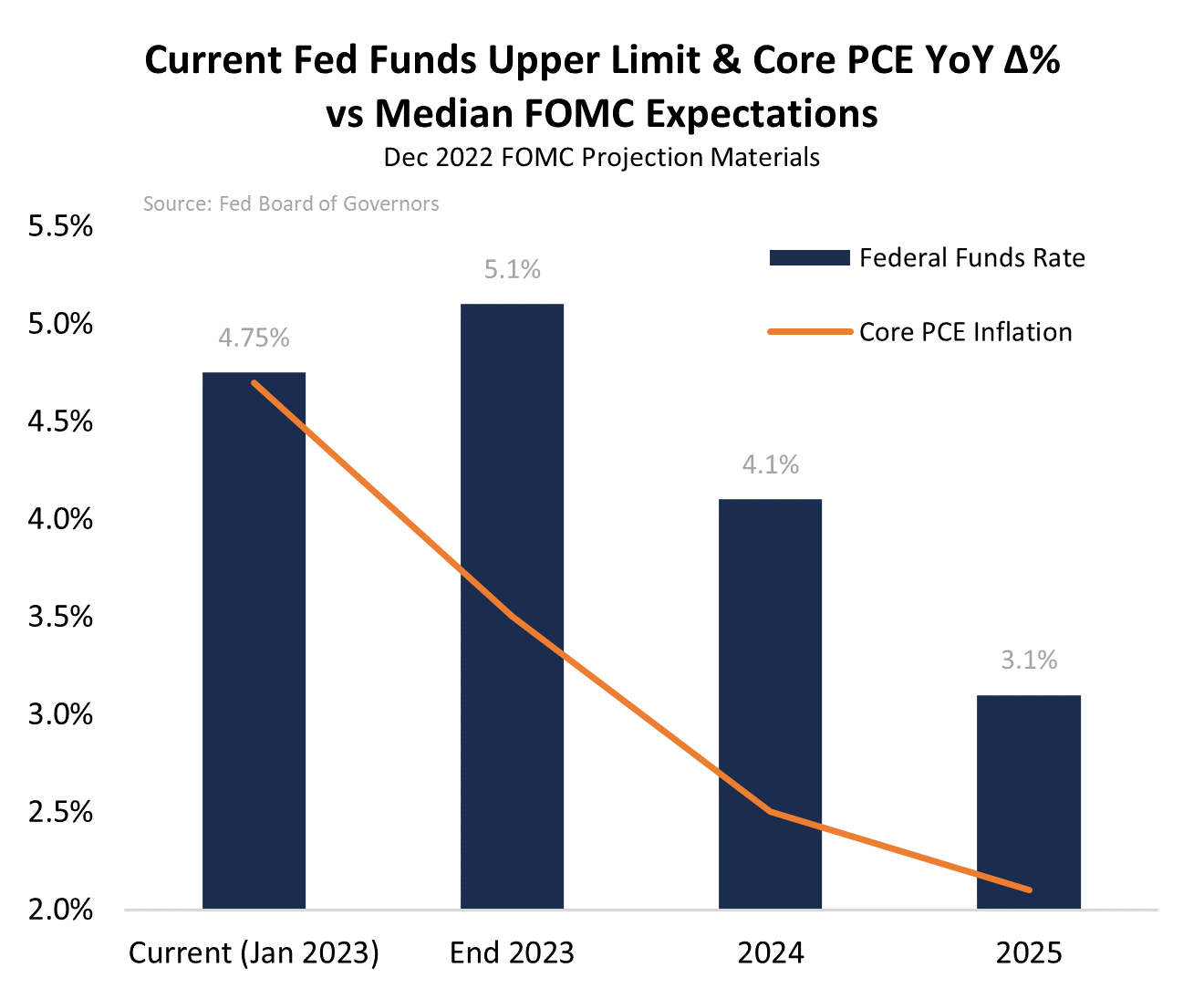

Though stocks and other asset classes rallied into the new year, markets gave up some of those gains in February, as the S&P 500 fell by -3.5% for the full month. That decline coincided with a spate of data that signals the rest of the first half may not be a better environment for equities than experienced in 2022. It has been just under a year since the Federal Reserve embarked on its ongoing monetary tightening cycle, which has already boosted the benchmark fed funds rate from near zero to an upper limit of 4.75%. Such a rapid pace of rate hikes has not been seen since the 1980s and, moreover, officials indicate that there are more to come.

The Fed’s most recent projection materials from December’s FOMC meeting cited a median terminal rate of 5.1% in 2023. However, recent economic data and comments from Fed officials indicate that rates will have to move even higher and potentially stay higher for longer. Fed funds futures contracts on the CME still suggests that the Fed’s policy rate will peak in the fourth quarter, likely at an upper limit of 5.5% – 75bps above current levels. Spreading that out over the course of the next nine months or so means that the pace of rate hikes will slow significantly compared to what markets witnessed last year. Already, the FOMC has wound down the size of its rate hikes from 75bps to 50bps, followed by 25bps at the most recent meeting. Assuming the central bank continues to move at that pace, the terminal rate suggested by futures markets could be reached by mid-year.

Though some have begun to speculate whether or not the expected terminal rate will need to rise, the more immediate issue impacting markets is whether the Fed will stick with its newly de-scaled rate hikes, or pump them back up to 50bps. That issue has cropped up following some less than ideal patterns in key inflation indices. In particular, the annual change in January’s headline and core CPI readings only fell by 0.1 percentage point each when compared to the prior month. Moreover, the core PCE index – the Fed’s preferred inflation gauge – actually re-accelerated by 0.1 percentage point. That’s not catastrophic for the Fed’s policy implementation, since inflation is likely well-past its peak at this point, but there are concerns that this gradual pace of disinflation is not happening quickly enough for the Fed’s liking.

That is a hard case to make, considering the Fed’s own materials suggest that they won’t get anywhere near their 2.0% target for inflation until 2025 at the earliest. By that point, the median point of the Fed’s own expectations suggest the fed funds rate will have been cut to 3.1% – well below where it is now. If anyone is taking the Fed at their word, the guidance they’ve issued suggests they’re prepared to be patient with inflation, rather than short-tempered.

According to minutes from the January meeting, there are “a few” Fed policymakers who’ve either remained adamant about sticking with 50bps rate hikes, or could have been convinced to support such a policy. But when it came time to make a decision, all twelve voting members of the committee were unanimously in favor of a 25bps hike. At least two vocal proponents…

To read the complete Viewpoint, current MRP Pro and All-Access clients, SIGN IN MRP Pro clients receive access to MRP’s list of active themes, Joe Mac’s Market Viewpoint, and all items included as part of the MRP Basic membership. For a free trial of our services, or to save 50% on your first year by signing up now, CLICK HERE